Viewpoint: A Regulatory Snapshot for Payment Services and E-Money in Europe

Payment opportunities in the EU come with complex requirements, which is why it’s important to understand the ever-changing legislative issues.

Payment opportunities in the EU come with complex requirements, which is why it’s important to understand the ever-changing legislative issues.

Let’s be clear: banks do a very difficult job – they store the value of society expressed as money. We trust them and they can’t get it wrong, but they are nothing but people and IT. Everything they own is on computer and they don’t like to take risks with this. Consequently, IT change for banks has been slow and safe. It has been incremental: bit by bit, byte by byte.

Historically, the large banks have been Lords of the Manor, between them owning every scrap of land as far as the eye can see. However, times are changing: invaders offering services the banks cannot provide as competitively have begun to disrupt the peace and take small pockets of land for themselves. Likening the march of the fintech new entrants to a land-grab by an invading force, the disruptors began with a neglected allotment here and there, then moved to take a meadow and now some are on the verge of swallowing up villages and small towns …

We recently surveyed more than 1,000 Americans about their payment preferences. The key trend that emerged: Traditional and emerging payments tools are being used together, not cannibalizing each other.

Like it or not, the bitcoin craze is here to stay. Over time, bitcoin will be a major disruptor in payments—with broad implications for governments, businesses and consumers. Burying your head in the sand is not an option.

A curious cultural shift is taking place when it comes to problem-solving in the financial services industry, writes Joe Channer The sector is not renowned as a home for co-operation: competition is intense, the stakes high, and individualism rewarded. Yet the industry has recently seen a marked increase in collaborative ventures. The post-crisis environment, with […]

There has been hype around wearable technology for some time now but only now is it reaching market maturity with the introduction and subsequent adoption by consumers of smart watches and wristbands. Just as we saw with smart phones and tablets, consumer technology, in this case wearables, has the potential to have a huge impact on the business world. The implications for the financial services industry are significant

The last lingering issue in the long-running legal dispute between merchants and the Federal Reserve Board of Governors over debit interchange fee caps took a step toward resolution this week, with the Fed detailing how it calculated a controversial aspect of the fee limit.

Sen. Richard Blumenthal (D-Conn.) this week sent a letter to the retail consortium Merchant Customer Exchange (MCX), which is readying the launch of its CurrentC mobile payments service, demanding details about its exclusivity policy requiring participants to block rival mobile wallets, along with other information.

BofI Federal Bank has received approval from the Office of the Comptroller of the Currency (OCC) to acquire certain assets and liabilities from H&R Block Bank.

The Office of the Comptroller of the Currency (OCC) has released new guidance for banks issuing tax refund-related products, including prepaid cards.

Connecting Governance, Finance, Risk & Compliance allows firms to govern all important issues and risks that exist at the intersection of multiple functions. Breaking silos and adopting a forward looking, holistic view of GFRC functions will be what provides financial institutions with a competitive advantage

Another warning to check that your vendors apply appropriate security measures.

Both Google and RadioShack are engaged in legal battles with consumers holding unused balances on the respective company’s gift cards.

The high street bank has always been relied upon to be one of those unchanging constants in our lives. Takeovers and scandals have come and gone, but the digital revolution has slowly changed the way financial products are delivered. Today the Internet, mobile devices and financial services have now converged to change the way consumers manage their finances and the way they connect with their bank

Regulations aimed at transparency across financial markets may be making things simpler for the regulators, but they are making life more complex for banks, according to Sven Ludwig, senior vice president, risk management and analytics EMEA, at SunGard.

At the SAP Financial Services Forum in London last month, the topic of digital transformation dominated the agenda. From legacy banks with lumbering IT systems to nimble fintech startups, the consensus was clear: The long-standing status quo is simply unsustainable in an increasingly digital economy

The only banking activity that is digital is taking money out of clients’ accounts, which is performed in real-time with 100% consistency. After that the banking journey is far slower and less consistent.

Look at most technology initiatives around you, most are obsessed with taking the cost out e.g. ATMs, online banking or selling more e.g. marketing automation, emails. As a business it’s important to manage the cost, but when cost becomes the primary driver, it creates more problems than it solves

While the role of bitcoin itself is still in question, there is a growing industry consensus that the blockchain—bitcoin’s underlying technology—may become to value, what the Web has been to information. And, the gift card industry may be the first to reap the benefits.

Despite the squeeze on capital created by the increased global regulatory burden, treasurers must still provide ample working capital for daily commercial flows, with minimum damage to their balance sheets. At the same time, the continuing rise in cross-border trade – frequently with relatively unknown and distant markets – increases exposure to geo-political and environmental risks. In such an environment, and particularly in light of post-crisis sensibilities, liquidity is more of a concern than ever, both to lubricate the daily machinations of trade and to act as a buffer for potential financial or supply-related shocks

Some cybercriminals are geniuses, I’m sure, but my recent personal experience with fraud suggests there is a gaping chasm between the promises of high-tech fraud-prevention methods and the existing, low-tech reality.

Contrary to popular belief, the financial sector is now far more aware and better prepared for cyber attacks. The Bank of England’s Financial Stability Report, issued 1 July, states that threat awareness has grown exponentially and the sector is leading efforts to combat cybercrime. Perhaps this isn’t surprising given 90% of large businesses across the sector had suffered a malicious attack over the past year. But what is worrying is that the financial sector is falling into a familiar trap: by focusing so much on defence, it has failed to make provisions for an effective recovery

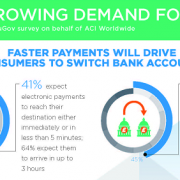

Faster payments could be the key factor in getting U.K. consumers to switch bank accounts, a new report says. In a study commissioned by ACI Worldwide, 45 percent of 2,000 of consumers polled in the U.K. said the prospect of faster and more convenient electronic payments would encourage them to consider moving their accounts to a different bank.

With governments, retailers, banks and (not least) consumers increasingly crying out for a means of confirming someone’s identity beyond any doubt, the search for a common, international standard of payment authentication is in full flow.

Over the past few years the financial industry has started to reinvent how it operates. Organisations are changing the way they serve their potential and existing customers, while maintaining the high levels of compliance and security that their customers and regulators require. The technologies available today mean that financial services organisations aren’t constrained in the way they once were. They can now access secure and compliant technology, on-demand, in the cloud which is helping them to create new ways to bring value to customers. But not all financial institutions have been able to take advantage of these technologies in the same way as newer entrants to the market have

A major online hacking forum and malware marketplace has been shut down in a coordinated operation by law enforcement officials in 20 countries.

The release in 2013 of Universal Rules for Bank Payment Obligation by the International Chamber of Commerce effectively endorsed and formalised the structure for international trade finance processes. Despite this, the volume of completed BPO transactions remains low

It’s now law, but not all of the act is in force yet.

Regulated entities that verify identity in connection with the issuance of stored value cards may find more flexibility in the principle-based approach to identity verification outlined in the proposed regulations.

As retailers prepare for the year’s biggest gifting season, there are some key principles to guide digital gifting strategies that maximize revenue and loyalty.

Public sector programs usually offer predictable loads and transaction volumes, and that information can be a plus. But reliable load patterns don’t guarantee overall success, especially if you price yourself out of profitability and sustainability.

Unless you’re a mathematician or a bitcoin fan, trying to understand what Ripple is—and why it’s so revolutionary—requires a bit of research (not to mention a double espresso!). That being said, here at Hyperwallet, we definitely think this new technology is worth investigating. In fact, I’d wager a bet that, within just a few years, Ripple could become as important to the world of payments as the Internet is to the world of information today.

The NBPCA’s newly elected president and CEO spoke with Paybefore about priorities, what happens behind the scenes of the association, and the work that lies ahead for an industry that must continue to raise awareness on the Hill.

Since the financial crash retail banks are faced with more regulatory and financial restrictions than could have been envisioned. This is coupled with increased levels of competition and much reduced consumer trust. Intelligent analytics may offer part of the solution.

Popmoney, Dwolla, Square Cash, Funding Circle, Venmo, Nutmeg, Transferwise, Stellar, Kabbage … this is not a list of the latest box office hits or some weird shopping list, but a handful of the emergent FinTech companies that are sprouting up everywhere like wild mushrooms. These companies are, to a certain extent, beginning to reshape and […]

It seems not a day goes by without seeing those three little letters and five numbers – ISO 20022 – appearing in headlines or articles. But hang on a minute, what’s all the commotion about? It’s just another message format that I need to make sure my systems can handle, right?

Chris Larsen, chief executive of Ripple Labs, talks about his concept of the Internet of Value, and why his company is not a disruptor …

Cloud-based technologies are spreading rapidly through the business world: the research firm IDC expects the cloud software market to be worth more than $100 billion by 2018, implying compound annual growth of more than 21%, roughly five times faster than traditional packaged software. It is clear that cloud computing is on course to become an […]

Cybercrime investigators from six European countries joined forces and recently busted a large gang of cybercriminals that had used malware in a widespread attack on online banking systems across the Eurozone, resulting in losses of at least €2 million (US$2.22 million), according to Europol, the EU’s law enforcement agency.