Industry alignment or industry confusion – what is a financial institution?

How industry labels and market segment boxes are no longer so revealing.

How industry labels and market segment boxes are no longer so revealing.

With the PSD2 compliance deadline having just passed, in this series we speak to some of the relevant firms both in and out of the U.K. about what this means for them and how the industry should move forward. In this installment, Finovate speaks to Brian Costello, Chief Information Security Officer, Envestnet | Yodlee about what […]

Five key myths have been allowed to percolate in the minds of consumers and it’s high time these were busted.

How to ensure the success of innovative new solutions is assured.

Insurtech will bring about new ways of broking and enhance the current insurance industry.

The explosion of e-commerce has led to an increase in online fraud and money laundering.

Let’s take a look at some of the key talking points of the cryptocurrency economy in 2018.

With more and more regulations being added and enforced, how can companies keep up?

How to stay competitive among other brick-and-mortar operations.

Lotto games have been around since before 205 BC in China, and used to finance major infrastructure projects.

Thanks to the internet and tech anyone anywhere can take part in financial trading.

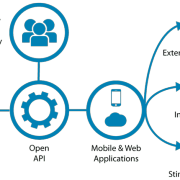

The arrival of open banking will (eventually) prompt entirely new services.

The landscape for financial services is changing, and the jury is still out on how the endgame is going to play out.

2017 will probably be noted for two things – Donald Trump took office and the world took notice of cryptocurrencies.

Explore the crucial elements of an effective digital strategy.

What does 2018 have in store for AI, and how can companies get the most out of it?

Blockchain still has the subject of heated discussion and massive investments of time and money.

Spirios Margaris discusses the troubling future of zero fee financial services.

A chat with Jennyfer Yeung-Williams, head of UK and European partner engagement at MunichRe Digital Partners.

What trends will be impacting the payments industry this year?

Reading smart books and applying other successful investment strategies will not lead to success.

They have deepened and broadened, now covering more services than have been traditionally associated with the term.

Cast your mind back to 2017. Did the trends predicted shake the industry as much as we thought?

Driverless cars; opportunity for the insurance sector or a challenge that could lead to its downfall?

How to tackle inequality and promote women in fintech.

InsurTech Bytes, the specialist InsurTech podcast series, speak with Allianz about their business strategy.

The digital currency is making a surprising entrance into the mainstream financial world.

The next wave of technological transformation will be driven by the rise of wearable technology.

It’s time to think out of the box when it comes to regtech.

Collaboration is the name of the game for regtechs trying to get ahead, according to Chris O’Driscoll of PA Consulting.

Implementation of first uses cases around real-time contextual added-value banking notifications and offers to make their appearance in 2018.

With wildly conflicting views from experts on the topic, and given that most of us had our first interaction with artificial intelligence whilst watching The Terminator, it isn’t hugely surprising that there is a fear of the rise of the robots.

In 2027, how will the insurance industry have changed?

How can women breaking into the FinTech and InsurTech industry get ahead?

2017 has been another eventful year for the payments industry. From celebrities like 50 Cent getting involved (more on this later) to businesses neglecting the needs of pretty much every generation bar millennials, there hasn’t been a dull moment.

The ability to blend artificial intelligence (AI) and human interaction should resonate strongly with financial service organisations due to their need to be highly targeted and responsive. When you provide the right service to a consumer at the right time, you can affect their behaviour and give them the push needed to complete the purchase.

The desertification of local banking is shifting the burden of live consumer interaction to contact centres. The question is: are your agents ready to become customer-facing bankers?

Walk with me through the seven levels of the Candy Cane forest, through the sea of swirly-twirly gum drops.

Recent hacks and data breaches have shown that cybercriminals are tenacious, smart and well resourced.

The recent surge in its price is good news for investors, but perhaps a death sentence for its functional value.