Interview: Roderick Simons, CTO of Yolt

What is it like to build a smart thinking money app from the ground up?

What is it like to build a smart thinking money app from the ground up?

Open banking is the future where everyone can win.

Dive into all things fintech!

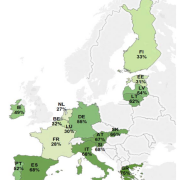

How many payment institution (PI) and electronic money institution (EMI) licences were granted in Europe?

Frankly, the time to act is now.

The NextGenPSD2 Implementation Support Programme (NISP) now has over 20 member organisations.

For those banks struggling with the complexities of PSD2 help is at hand.

Interview with Javier Santamaría, chair of EPC, to mark the first anniversary of SCT Inst.

Current regulation makes reporting inefficient and discourages communication, EBF says.

Realising the benefits that Open Banking will deliver will take time.

Italy’s Banco BPM has selected Worldline’s Cristal for its instant payment platform.

The Baltic nation sets out its ambitions to be the region’s fintech hub and gateway to Europe.

What are the options for the 8,000 firms that use EU financial services passports to do business in the UK?

A head of steam is building around regtech, driven by the confluence of interest from regulators, banks and fintechs.

All enabled via its partnership with WeGift.

It’s crucial for organisations to look at this fundamental regulation in a holistic manner.

Whatever happens in the coming year, there is a wealth of opportunities for fintechs to pursue.

The new service is “industry-first”, according to Form3.

Common standards for secure data exchange and robust authentication of PSPs’ interfaces are needed.

The requirement to repaper legal documentation must now be treated as business as usual.

Catch up on FinTech Futures’ top five fintech stories of the week – all in one place!

Everyone be cool. This is Brexit.

How to harness the opportunities presented by tech-driven innovation in financial services.

Ten facts and figures celebrating SEPA’s achievements.

The banking technology sector suffers from skills shortages and relies heavily on foreign nationals.

The payments industry was dragged kicking and screaming into the single euro payments area (SEPA), but on 28 January 2018, the initiative will celebrate its tenth anniversary. No doubt former doubters will sing its praises.

How to be a sore loser.

Catch up on Banking Technology’s top five fintech stories of the week – all in one place!

An overview of the most important threats in the payments landscape.

PSD2 comes into force on 13 January 2018. It aims to open up the European payments market to greater competition and transparency, but its effect will be more far-reaching, acting as a catalyst for innovation not just in payments, but in the wider financial services market.

Catch up on Banking Technology’s top five fintech stories of the week – all in one place!

The European Central Bank (ECB) conducted a comprehensive study to analyse the use of cash, cards and other payment instruments used at points of sale (POS) by euro area consumers in 2016.

Catch up on Banking Technology’s top five fintech stories of the week – all in one place!

It may not provide all the ticks on everyone’s wish list, but the new SEPA Instant Credit Transfer Scheme (SCT Inst) could well be the start of something even more seismic for the European payments sector and also pave the way for a different, more immediate way of conducting business.

Fiorano Software, a specialist in integration middleware and API management, has launched Fiorano PSD2, a solution enabling banks to comply with the European Union’s PSD2 regulations.

This free white paper discusses the implications of PSD2 from an end-user standpoint.

There is intense interest in instant payments (IP) throughout Europe. Domestic schemes are already live in the UK, Denmark, Poland and Sweden. The success of these schemes shows what’s possible but also teaches many lessons.

The European Central Bank’s (ECB’s) governing council will decide by the end of this year whether to greenlight a new real-time gross settlement (RTGS) system to replace the decade-old Target2 platform.

We live in impatient times – everyone wants to be able to pay who they want when they want, instantly and regardless of location. The UK has had instant payments since 2008; Faster Payments volumes have exceeded all predictions and now exceed 135 million per month.

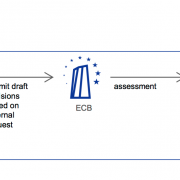

The European Central Bank (ECB) has published a guide to assessments of fintech credit institution licence applications.