Infographics: The world of e-commerce

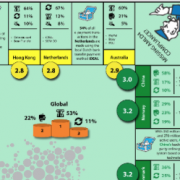

Did you know that in the Netherlands 54% of all transactions are carried out using the iDEAL online banking system? Or that Germans prefer to pay on account via direct debit and the popularity of e-wallets is growing in Russia? ‘The world of e-commerce’ reveals the three most popular e-commerce payment methods across 22 countries […]