Viewpoint: Enough with the 2016 Predictions—Let’s Think Bigger!

Forget predictions. We’ve got work to do. There are several significant challenges for payments that need to be solved from fixing cross-border payments to making payments disappear.

Forget predictions. We’ve got work to do. There are several significant challenges for payments that need to be solved from fixing cross-border payments to making payments disappear.

With more contactless cards in the U.K. than people, the new age of payments is already here. But we’re not done yet, and thanks to biometrics, we could be the next form factors.

While mention of bank robberies will often conjure images of masked criminals and high-speed car chases, most modern instances of the crime are being conducted from behind computer screens. In addition to the lure of stealing cash, these criminals are going after banks for valuables such as the personal data of customers, details of mergers and acquisitions between companies and the private tax information of corporations, data is fast becoming an incredibly valuable commodity in its own right

New peer-to-peer platforms that match lenders with borrowers are proving to be more efficient than banks at connecting those with money and to those that need money. Known as marketplace lenders, this new industry is still very much in its infancy, currently representing a tiny proportion of total loans compared to bank lending

To kick off the New Year, we asked payments industry thought leaders to tell us what happened in 2015 that will most influence payments in 2016 and to discuss their hottest priorities for the next 12 months. Responses run the gamut from a combined Visa/Visa Europe to compliance, wearables and the impact of Chase Pay.

Aspiration doesn’t look like it used to. The face of Eighties ambition was a power dresser, clad in a suit with shoulder pads as they rushed to Wall Street to earn as much as they could, whereas today’s bright young things are more likely to be found sipping lattes at a co-working space in Silicon Valley

There’s no questioning the popularity and appeal of gift cards—especially during this time of the year. Giving recipients the ability to treat themselves to something they really want or need has become prized among gift buyers. What’s even more exciting is how the concept of gift cards continues to evolve as new brands and card types launch.

The CFPB needs to return to its original plans on prepaid regulations and put its proposed rules on a New Year’s diet. By issuing rules focusing solely on disclosure, the CFPB could issue guidance earlier in 2016 that would help consumers, prevent access disruptions, and potentially reduce the size of the landfill needed to for the mountains of noncompliant cards and marketing materials.

The distributed ledger – the central nervous system of the Bitcoin system – is the most sweeping departure from the long-standing financial bookkeeping practices followed since the codification of the Medici’s double entry accounting system.

If 2015 is to be remembered as the year regulators challenged boards to demonstrate their strong governance over their risk management, 2016 promises something just as important. In fact, 2016 will arguably be a truly momentous year in the world of non-financial risk as it could well become the year that risk governance silos are finally dismantled

Millennials – those highly sophisticated, tech-savvy men and women born between 1980 and 2000 – present enormous opportunities for banks and other financial institutions. Yet to be successful, these businesses must understand and meet the needs of a generation that grew up having it all, seeing it all, and being exposed to it all since early childhood – and that is no easy task.

Outdated legacy IT systems are a major stumbling block for traditional UK high street banks as they look to fight back against their often more agile rivals, widely known as ‘challenger banks’, who unhindered by complex, unwieldy IT infrastructures are typically better positioned to innovate.

Churn is by far the biggest challenge facing prepaid debit card companies. Issuers can combat it by tapping smartphones and real-time analytics to deliver personalized services through a preferred communication channel.

Poor user experience with EMV could be a boon for contactless cards and NFC mobile payments. But retailers could take immediate steps to improve the UX with contact EMV, starting with cashier education.

When it comes to the payments, there are more choices than sweet treats at Dylan’s Candy Bar in NYC (i.e., the world’s largest candy emporium!). The payments landscape is likely to become increasingly confusing and fragmented as retailers ramp up their efforts to influence buying decisions. If we don’t help our members evolve and understand how things are changing, credit unions risk losing the transaction and engagement.

Digital technology is on the verge of transforming banking, in a similar way that Spotify has completely changed the music industry and Netflix has revolutionised broadcast entertainment

Employment prospects in the UK finance and banking sector in the New Year are the brightest in the past three years as high profile data breaches, such as those at TalkTalk and Sony, create a surge in demand for cyber-security experts.

2015 has been a year of extensive discussion about what role blockchain can play in making processes in the financial services industry more efficient. It has also been a year where both banks and start-ups have been testing whether distributed ledger technology can adequately replace costly legacy systems and improve securities processing, writes Brian Collings. […]

As part of the ongoing Basel reforms, the Bank for International Settlements is busy rewriting the rules that govern how much capital banks must maintain in order to mitigate different types of risk. So far the Standardized Approach for Measuring Counterparty Credit Risk Exposures and the Fundamental Review of the Trading Book have garnered the most attention. However, these are just two components of a much larger package of changes to the Basel capital requirements, which banks need to think about holistically and start factoring into their technology programs now

Quick business successes can be built on the UK’s payment system that will play a key role in encouraging the efforts required to ensure that it achieves the “world class” status the industry is aiming for.

Integrated stress testing is the preferred tool from a supervisory perspective. And that’s on a global basis. It may not be new, but it is featuring increasingly higher on the regulatory agenda and so understanding the technological opportunities is all important. A key building block for effective and integrated stress testing is an integrated balance sheet strategy

There is an uncanny similarity between Prime Minster David Cameron’s emphasis of moving from a “low wage, high tax, high welfare society to a higher wage, lower tax, and lower welfare society” and a shifting focus among the asset management community.

It should be no surprise to anyone that gift cards are forecasted to be uber popular again this holiday season. However, it will be crucial for those in the prepaid industry to be mindful of plugged-in shopper preferences to capture holiday spend.

Knowing your customer is taking on new meaning for retailers, If you want to thrive, you must give your customers a personalized shopping experience with a simple integrated payments process.

In 5 years plastic cards will be dead! A bold prediction for sure and likely one you’ve heard in any of a dozen payment mixers you’ve attended over the last year. But for our restaurant brands, we see a more nuanced picture that requires us to execute a simple, perhaps obvious, formula.

The five most important takeaways from Money20/20 that will shape payments for the foreseeable future.

Craig James explains how passporting with an e-money license allows U.S. prepaid companies to conduct business in EU countries.

Banking and disruptive change go hand in hand. There was the era of deregulation. Then the 2008 crisis and the era of re-regulation. Then PPI. Now there is digital, and no sector is secure from its transformative power, not even a heavily fortified one …

In this age of tablets and smartphones, customers expect instantaneous access to information and services. Emails, tweets, shopping: everything is now real time or forget about it. As a result, instant payment is upon us, writes David Andrieux. Benefits of instant payments aren’t hard to see. For the economy, they allow consumers and businesses to […]

There is no doubt that IT and IT projects are becoming increasingly critical to banks’ success, yet a recent survey by Accenture found that only 6% of the directors of the world’s largest banks have any IT experience …

The UK’s payments system infrastructure is widely recognised as market-leading. However, evolving customer expectations and innovation in the fintech sector dictate that now is no time to rest on laurels. Work must begin today to develop the payments experience that will be taken for granted in 20 years.

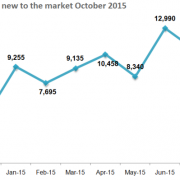

The news of major lay-offs to come put a dampener on otherwise good news in the financial sector jobs market in the UK last month. According to the Morgan McKinley London Employment Monitor, October saw an across the board increase in both new job opportunities and new job seekers.

Recent years have seen unprecedented changes to the technical infrastructure of financial institutions. Many of these changes have been driven by regulatory mandates drawn up in response to the financial crisis of 2007/8. As the Global Systematically Important Banks battle to comply with the January 2016 deadline of the Basel III Directive BCBS239, it is […]

Legislators and regulators are grappling with how to apply existing money transmitter laws to an emerging industry. Read about the challenges and latest developments across the U.S.

Eight years on from the global financial crisis, and banks continue to face a growing number of challenges. Many have ceased or significantly reduced proprietary trading, with the resulting reduction in both risk and reward. This period has also seen lower risk appetite among many investors and continuing global competition which has put pressure on profit margins,

From the very first coins changing hands in 700 BC, through to the Bank of England pioneering the first use of a pre-printed form – or cheque – in 1717, and the emergence of credit cards in the mid 20th century, how we pay for goods and services has continued to evolve. We now face a cashless society

The fact that London’s financial services sector is also a hot spot for technology innovation is not news. In 2014, investment in financial technology firms grew by 136%. Earlier this year, George Osborne identified London’s financial technology sector as a particularly bright spot in the recovering economy – not surprising when you consider the transformational effect that information technology continues to have on the industry

The selfie boom was born in 2003 with the world’s first front-facing camera, and millennials are the first generation to grow up with technology focused on one’s self, bringing new expectations to the meaning of personalized, digital services.

Personalization has become more important than ever to consumers, as they shun anonymous mass advertising in favor of individual reviews and one-to-one brand engagement. But what if instead of helping big brands to adapt, you were to lead the change? This is where competitive advantage comes to life.

Clearly there’s an issue with how banks manage cross-border money transfers and payments. The process is inefficient, costly and archaic. That being said, I can understand why it is the way it is—building a truly global platform that enables FedEx-like payment transfers is no easy feat.