Fintech: beware the fake news

Ben Robinson, Temenos

In every aspect of life, sentiment overshoots. We overbuy and oversell securities. The political pendulum swings from left to right. Shops run out of ultra-fashionable goods only to heavily discount excess stock a couple months later.

Ben Robinson, chief strategy officer at Temenos, explains how this is not a new phenomenon, but has got worse in our attention economy, where we live in echo chambers and where there is a general tendency towards sensationalism.

From hyperbole to despondency

Fintech is one such example of where sentiment overshot. A few years back, the general consensus was that banking as we knew it was over. Technology change, in particular in the form of smartphones, big data and cloud, had allowed anyone to create a fintech start-up, distribute services directly to consumers (or create a platform for consumers to provide those services to each other) and offer a richer customer experience. So banks would soon hemorrhage market share. A Telegraph headline from mid-2015 captures the mood, “Banks should be afraid, the disruption of financial services has only just begun.”

Fast forward two years and opinion has arguably swung too far in the other direction. The consensus now is that fintech firms tried to disrupt banks but couldn’t. Flagship fintech companies were bought up (like Simple), embroiled in scandal (Powa Technologies,), listed in IPOs that subsequently bombed (Lending Club) or ended up partnering with the banks they were supposed to disrupt (Moven). As the NY Times put it in a headline from earlier this year, “Silicon Valley tried to upend banks. Now it works with them”.

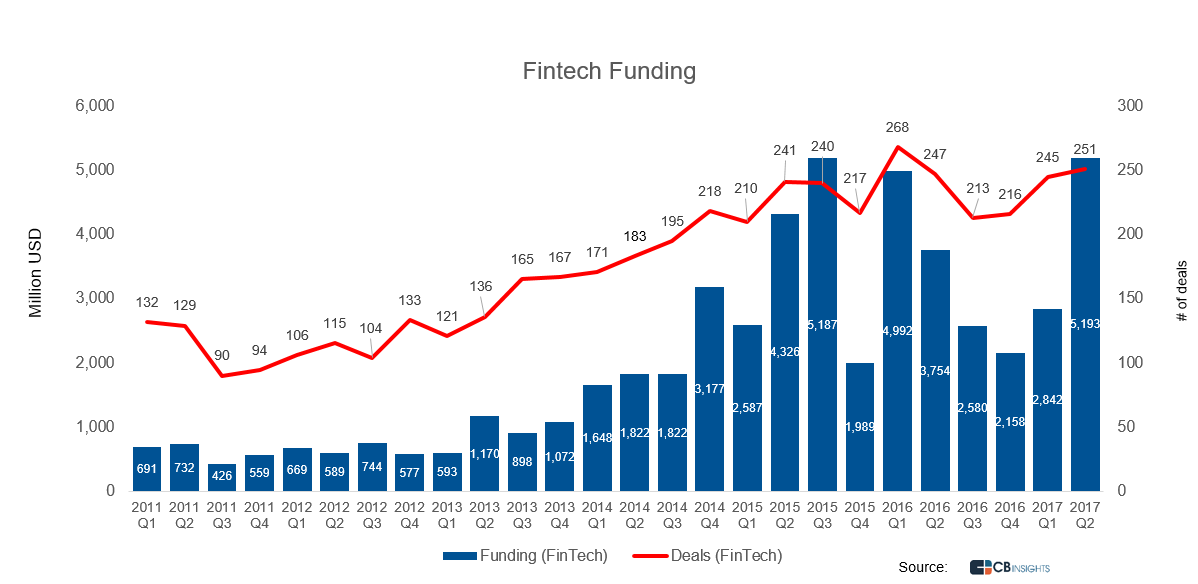

If we were to apply Gartner Hype Cycle terminology to fintech in general, we would argue that fintech went from the peak of inflated expectations to the trough of disillusionment in the last two years. If you look at the investment figures, however, the picture is not so clear. While there has been a correction in VC funding, Q2 2017 was the largest quarter of investment yet. Maybe Q2 was a blip, maybe we are heading out of the trough of disillusionment to the slope of enlightenment – or maybe investors are more sanguine about the prospects for fintech, seeing through the hype cycle.

Fintech has had a profound impact

The truth is that fintech is neither going to kill all banks nor is it a fad. For sure, fintech firms have so far taken little market share – just 2% according to a recent report from the Economist Intelligence Unit (EIU). And we are likely to see a massive thinning-out in the ranks of c. 20,000 fintech companies in the coming years. But the pessimism has become exaggerated for four main reasons:

1. Some extremely successful and highly disruptive fintech companies have been born, such as Ant Financial and PayPal (which, if a bank, would be one the ten largest in the US);

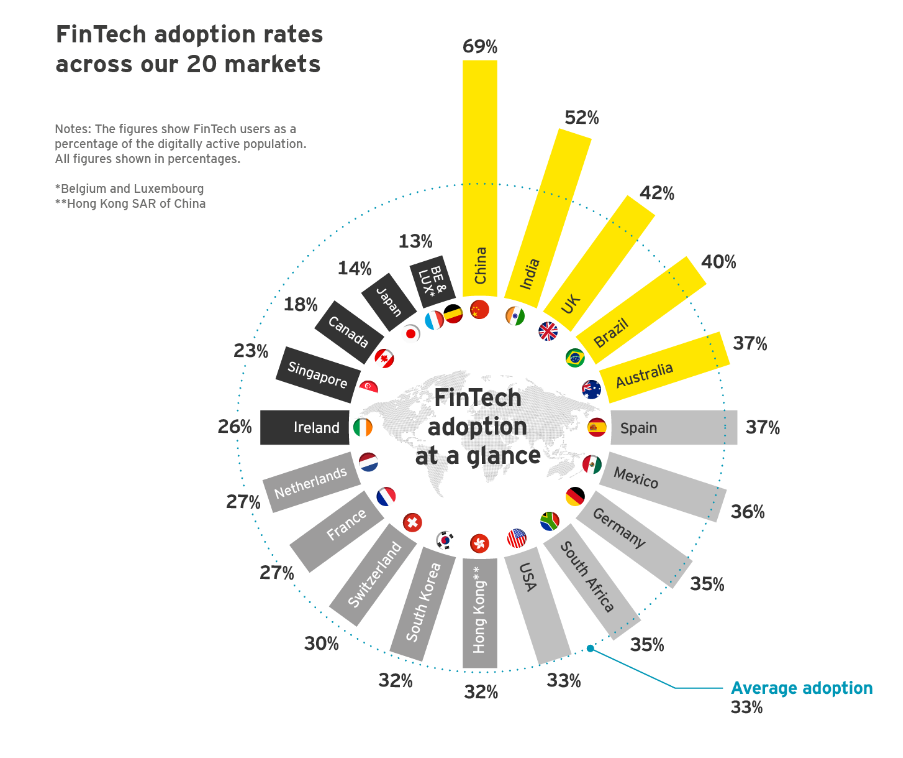

2. Adoption rates for fintech products are growing and are already material in many countries around the world (see chart below), meaning that fintech firms are successfully changing customers’ banking habits, which should help lower the cost of acquiring customers in future (a key hurdle for many fintechs);

3. Fintech companies are evolving, pushing further in middle and back office functions, extending the range of services they offer and generally becoming asset heavier and more vertically integrated, putting them in a position to compete more effectively; and,

4. Because the indirect impact of fintech has been massive.

Since fintech start-ups started to proliferate at the start of this decade, we have seen major indirect effects on banks. They have been forced to become more innovative (see later), introduce product and service improvements and lower spreads. Although very difficult to isolate the impact, it is uncontroversial to assert that tougher competition from fintech firms has adversely impacted bank profitability and that the impact on profitability has been significantly bigger than the impact on market share, especially since fintech companies have to date disproportionately targeted high-margin areas like FX transactions and unsecured lending.

Is fintech that innovative?

Much of the discussion about fintech gets framed in the simple and reductive notion that fintech firms bring all the innovation to banking (and, thus, banks must partner, buy or copy fintech innovations to protect market share). But we must ask ourselves whether fintech is really that innovative and if banks can still innovate.

Clayton Christensen, Harvard Business School professor, and an authority on disruption, talks about three types of innovation: 1 – “empowering innovations”, which democratise consumption by taking expensive goods and making them cheap enough for a wide variety of consumers to afford, such as Ford’s Model T. These innovations create jobs and consume capital; 2 – “sustaining” innovations, which essentially replace old products with new models, such new ranges of cars.

Christensen argues that “sustaining” innovations keep economies vibrant and account for most innovation, but since they are largely zero-sum (we replace one car with another, not adding to the overall stock of cars), they have a neutral effect on economic activity and on capital; and, 3 – “efficiency” innovations which reduce the cost of making and distributing existing products and services. These reduce employment and free up capital.

If we look at fintech innovations through the prism of Christensen’s innovation framework, it is evident that most fintech innovations are either “sustaining” or “efficiency” innovations. They are providing consumers with better alternative services and also lowering the cost of banking, both of which improve consumer welfare (in economic parlance, reducing the dead weight loss or growing consumer surplus). Further, if they are efficiency innovations, they are helping to allocate capital to parts of the economy that are more productive given, as argued in a previous article, banking in developed countries is oversized relative to historical norms and relative to what is economically or societally optimal. Former Barclays CEO Antony Jenkins recently estimated that the number of people employed by banks could fall by 50% by 2025.

Banking – catalysed by the fintech movement – is essentially going through a digital upgrade which will result in a shake-up of the value chain and emergence of new business models. But is doesn’t follow that it will necessarily result in the “empowering” innovations that are so economically and socially beneficial.

Cryptocurrencies are likely more disruptive

There do, however, seem to be (at least) two exceptions.

The first is mobile banking in the developing world. This innovation, by both lowering the cost and overcoming the physical impediments of supplying financial services to the unbanked, has the power to be truly empowering.

Innovations in wealth management may also be empowering if they are able to firstly bring retirement saving to a much wider demographic and better match the assets to the needs and risk profiles of investors.

But the other clearly empowering innovation is around cryptocurrencies and their attendant technologies. This is somewhat ironic since even more so than fintech generally, cryptocurrencies have been subject to the ebbs and flows of popular sentiment.

Where once people thought cryptocurrencies were the preserve of criminals dealing anonymously on sites like Silk Road, increasingly we glimpse the possibility for major innovation.

Many of these innovations may be “efficiency” innovations, removing intermediaries from existing, complex financial value chains. One example would be if central banks were to introduce Cryptocurrencies, which as Marilyne Tolle from the Bank of England states, could lead to banks “becoming pure intermediaries of loanable funds”.

But others are likely to be “empowering” innovations stemming from two very important characteristics of cryptocurrencies: the shared data ledger and the tokens that can be created on top of the protocol. These promise to make it easier for new companies to raise money and gain clients, to increase the return on innovation and to break the dominance of the largest platforms.

In its must-read essay “Fat Protocols”, Union Square Ventures explains the importance of shared data: “By replicating and storing user data across an open and decentralised network rather than individual applications controlling access to disparate silos of information, we reduce the barriers to entry for new players and create a more vibrant and competitive ecosystem of products and services on top.”

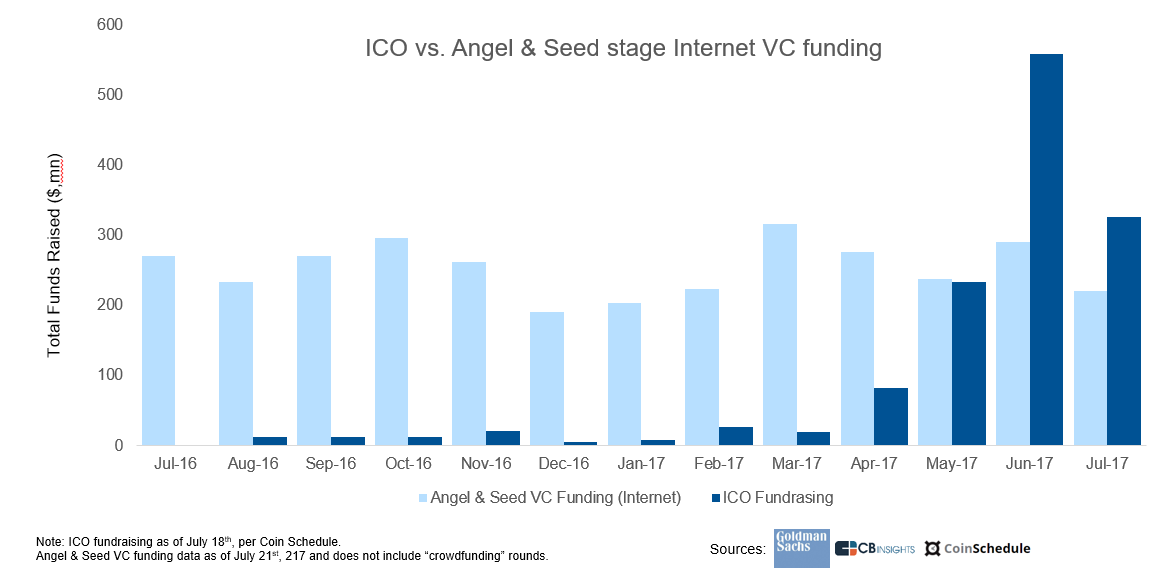

In terms of cryptographic tokens, these are important because they create a means for developers to monetise protocol innovations, Increasing the incentives to innovate, as well as a means to fund development. But the benefits go beyond just monetisation and funding. As the recent buzz around initial coin offerings (ICOs) illustrates, with token sales companies can generate working capital at the same time as building an ecosystem of suppliers and buyers that might otherwise take a long time or be difficult to create, giving an early and important boost to the business. (Tokens may also improve valuations by opening up a wider pool of investors and offering a liquidity premium, although some commentators are more skeptical about this.)

History will almost certainly show the market for ICOs is currently in a bubble territory and, if so, growing regulation is likely to be what punctures it. But, tokenisation represents a major shift both in how firms raise money and how innovation gets rewarded. The US Securities and Exchange Commission (SEC) in its recent ruling called it a “new paradigm”.

Whereas fintech promises to upgrade banking for the internet age, cryptocurrencies offer the possibility of an internet of money.

Can banks innovate?

Many people think that big companies can’t innovate. Not only are they too bureaucratic to innovate, they say, but it is not in their interest to do so. Stock prices, pay and other corporate mechanisms create a strong bias against introducing game-changing, empowering innovations.

The problem with this opinion is that, even if it might once have been the case, it doesn’t seem to hold true anymore. If we look at the tech space, for instance, there have been several empowering innovations over recent years, such as cloud computing and smartphones, and these have come at least to the same extent – if not to a greater extent – from large companies.

Big firms have many advantages in the digital age on which they can capitalise – especially if they are prepared to adopt open models (which many are) and can put into place start-up-like practices (which many are doing). Large firms have the capital needed to roll out game-changing innovation, the customers who will adopt it and the data to underpin it. In contrast, the falling cost of innovation acts as a double-edged sword for start-ups: easier to come up with new ideas, harder to implement them before others copy.

It is not surprising, then that much of the innovation in banking is now coming out of large banks. Commercial Bank of Africa was not the first to launch mobile banking. But, through a mixture of technology know-how, an existing banking licence, the power to forge the right partnerships and the capital to roll out the service across multiple countries, the mobile bank it launched at the end of 2012 – M-Shwari – now boasts over 27 million users, making it the largest bank in Africa by customers. And it continues to innovate, leveraging APIs to offer third-party services to its customers, such as healthcare, insurance and device-financing.

Are all banking business models in need of an upgrade?

In 2010, my colleague and I had a detailed look at the Metro Bank strategy. This was the first new retail bank to launch in the UK for over 100 years. And, essentially, it sought to take a business model that had been highly successful in the US with Commerce Bank – centered on maximising deposits per branch – and apply it in a new country and in a digital era. Like many others, we weren’t sure that it would work (our report was entitled, “Breaking the mould, but breaking the malaise?”).

Seven years on from its launch and Metro Bank is flying. It has a million customers, it is growing revenues at 50% per annum and profitability is beginning to take off. The key to its success: maximising deposits per branch. Because as its founder Vernon Hill told me in 2010, “once deposits per branch hit the $30-40 million mark, costs stabilise and marginal profit explodes”.

Bringing balance to the debate

The Metro Bank case is an apt place to draw a conclusion. Banking is undergoing a major upgrade for the digital age and new, networked business models will emerge. Fintech start-ups are playing a major role – especially indirectly – in bringing about that upgrade. But, banks can still innovate and will likely bring about some of the most profound innovations. And not everything will change. As Metro illustrates, while network effects (or demand-side economies of scale) are becoming increasingly important, supply-side economies of scale still matter. While the distribution of banking is becoming increasingly digital, there is still a place for physical interaction. And while people likely to proclaim the death of banking or the death of fintech, reality is always more balanced.

By Ben Robinson, chief strategy officer at Temenos and co-head of Temenos Marketplace.

Banking Technology Awards 2017 are open for entry!

Know any innovative products, inspirational projects, skilled teams or visionary leaders that deserve a special recognition this year? Nominate them for a Banking Technology Award!

Deadline for submitting the nominations has been extended to 8 September 2017.