How the fintech sector can navigate the winds of change in the UK

I’m sure, like me, that you set an early morning alarm on 31 January in keen anticipation of the publication of the UK Labour Party’s plan for financial services.

There’s an opportunity for forward-thinking companies to help shape the future of UK fintech

The UK polls suggest that Labour are by far the most likely winners of the next general election, which can now only be months away. Market observers, investors and fintech executives have been keenly scanning their policy output for indications of their intentions and what a potential Labour election victory could mean for fintech in the UK – and further afield.

I believe that the fintech industry has been looking for some leadership, or at least a definite steer about what the UK fintech space will look like in five years. Everything in Labour’s report – titled ‘Financing growth: Labour’s plan for financial services’ – is qualified, hedged, risk-averse and with no identifiable timetable. You can read this report cover-to-cover and still be uncertain about what the first year of a Labour government will mean for financial services.

Compliance professionals hoping to be proactive and thorough, as the current law requires them to be, may be worried.

However, across the six key objectives outlined in the report, there is a common theme in that there are multiple references to reforming regulation to simplify and improve the landscape, while also offering consumers regulatory assurance that is more in tune with the technologies of the 21st century.

A “growing dissonance”

Earlier this year, Paysafe’s chief risk and compliance officer Richard Swales was quoted in the Irish Independent as saying there is a “growing dissonance” in regulatory approaches between Europe and the UK at an industry event in Northern Ireland.

For companies like Paysafe that operate in both markets, this could result in a complex and often duplicated compliance requirement. This is a key point within Labour’s report, highlighting the need to try and work more collaboratively with international partners on regulatory issues, most prominently the European Union.

The reason this caught my eye is because, in a FinTech Futures video published last year, I had cited ‘glocalization’ as one of the big trends to come in fintech – the idea that, while technology might be ubiquitous, it all has to be wrapped around the different regulatory requirements of each jurisdiction that you intend to operate in, making for a fragmented business model.

But that brings us to the Brexit-shaped elephant in the room. The fact that Labour will not seek to rejoin the EU is given a prominent position and highlighted with bold text in the report, underlining its political importance. However, careful observers will note that this does rather call into question what exactly ‘deepening cooperation’ will mean in practice, alongside a mysterious promised organisation called the Regulatory Innovation Office.

When reading the report, it gives us an opportunity to compare the UK context with that of other fintech centres like Dublin. As Dublin has emerged as a key location for global tech companies, boosted by its tax policies, an associated payments industry has developed around it.

An opportunity for forward-thinking, entrepreneurial companies in UK fintech

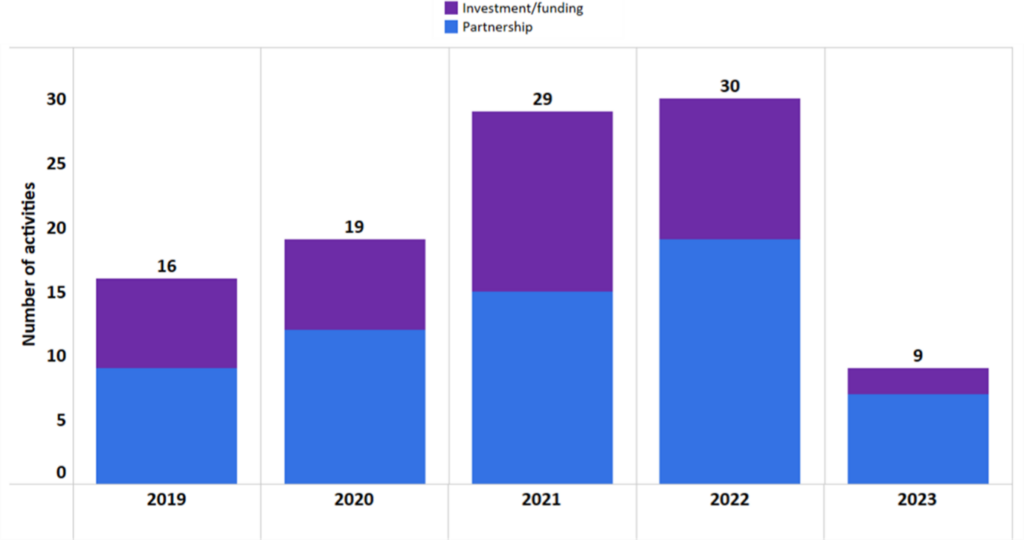

Nobody needs reminding that the fintech space has faced a number of challenges over the last two years. UK fundraising and deal volumes are all substantially down in Omdia’s neobank activity tracking data, and flotations have been declining. If Labour wants to deliver on its stated ambition of getting the UK back to being a fintech pioneer – and not just focusing solely on London, but by delivering fintech-friendly environments across all regions – then they need to resolve this regulatory issue.

Investment/funding and partnership activity by neobanks in the UK. Source: Omdia’s neobank activity tracker

Uncertainty is the thing that will hold the UK back more than anything else. Uncertainty means that fintech entrepreneurs, investors and consumers will be put off and driven away. Meanwhile, countries like Ireland are cementing their lead in the fintech space.

All of the factors that make it difficult for businesses to operate in both the UK and the EU may simply result in companies leaving the UK altogether if the situation does not improve rapidly. If anything, this underscores the necessity for fintech companies to do their own work in this area. Relying on the political classes to set out a roadmap for the future of UK fintech, as important as policymakers are, looks to have very little reward.

There is an opportunity for forward-thinking, entrepreneurial companies to force the ground in UK fintech, to shape the market in ways that would be difficult elsewhere. If political parties do not want to seize the moment and pose a radical plan for the future, then the industry needs to get back to some old-fashioned entrepreneurialism. The creation of the newly formed Unicorn Council for UK Fintech (UCFT) might be the first indication of fintech doing this.

About the author

About the author

Ouliana Smith is a senior research analyst in Omdia’s Enterprise IT Financial Services Technology team and has 10 years’ experience in financial services. Since joining Omdia in 2022, she has focused on digital transformation in retail banking and fraud solutions with a strong interest in alternative payments.

Ouliana started her career as an associate analyst with Datamonitor, now GlobalData, a global market intelligence provider, where she specialised in cards and payments before later moving into wealth management.

Ouliana holds a first-class honours degree in mathematics from Coventry University and an upper-second-class honours degree in art history from the Open University.