Millennials and Gen-Z embrace digital banking and “mobile-first” payment mindset. Could that be a problem?

We’ve seen rapid transformation within the payments and fintech space in recent years. New platforms on which customers can conduct business quickly and from any location are developing into the new standard for banking.

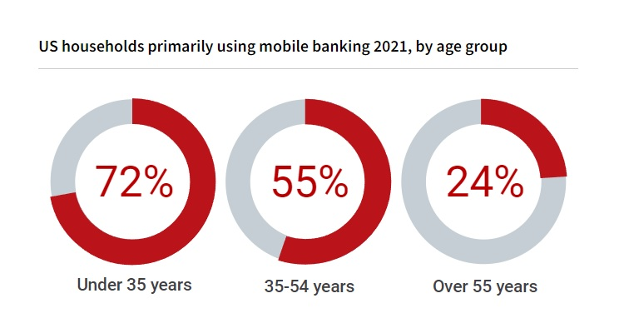

Looking at the recently released 2024 Cardholder Dispute Index, commissioned by Chargebacks911 in partnership with The Strawhecker Group (TSG), we see that banking customers under the age of 35 prefer managing their finances through a mobile app. This is highlighted when we compare them to customers aged 55 or over; younger users prefer mobile banking by a three-to-one margin, compared to older users. Nearly 72% of all consumers under the age of 35 prefer the app, compared to only a quarter (24%) of those aged 55 or over.

This suggests that younger customers are content with the mobile banking experience. And, as time passes, this will likely become the standard method through which people engage with banks and other financial services.

Mobile wallet adoption also shows continued growth

The report also finds that growing adoption of mobile wallets goes hand in hand with the use of mobile banking services.

It’s true that the portion of customers who’ve embraced mobile payments as their preferred option is still comparatively small. According to the study, roughly one in ten buyers prefer to opt for mobile wallet apps like Apple Pay or Samsung Pay. In contrast, 80% of respondents say they still prefer credit or debit cards. The remaining respondents were split between bank transfers, buy now, pay later (BNPL) options, peer-to-peer (P2P) apps like Venmo and Zelle, and cryptocurrency.

Again, though, we see use among young people being quite a bit above the trend line. Younger respondents were nearly three times more likely to favor mobile payments over conventional credit card payments.

As adoption of these platforms grows, we’re likely to see more and more people – especially Millennials and Gen-Z shoppers – make the jump to mobile payments as a first option. And, as those shoppers mature and become the dominant voices in the payments industry, their preferences will become the new norm.

What this means for the fintech space

So, what can we take from all these first-person insights?

On the one hand, it suggests a coming sea change in the payments industry. We expect that, within the next decade, we’ll see a seismic shift away from brick-and-mortar banking, physical payment cards, and other markers of legacy banking operations. In their place, institutions will shift toward providing digital-first, mobile-enabled experiences.

Major institutions in the banking space may be vulnerable to upstart fintech firms that are willing to meet the expectations of younger banking customers, if those legacy institutions are not willing to do so. As Millennial and younger customers age into demographic dominance, their preferences will come to define the standard for banking and payments.

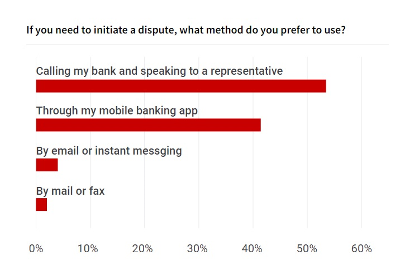

This carries both positive and negative ramifications. For instance, while a more digital-first approach will enable a better, more customised user experience, there’s also the risk that we may end up removing some quite useful friction points. For instance, going back to the report cited earlier, we see that mobile apps are the second most-preferred way of filing disputes:

As with trends we discussed earlier, younger bank customers tend to be much more likely to use an app to initiate a dispute, while older customers prefer to call. This isn’t a problem on its own. But, given that first-party misuse of the chargeback process may account for up to 75% of all chargebacks (according to Visa) the convenience of initiating a dispute in seconds via a mobile app is likely to cause problems.

Click on the image to download the 2024 Cardholder Dispute Index

It sends the message that filing a chargeback is a quick and easy way to “get something for free”. That’s not a message we want to send, especially when, as the 2024 Cardholder Dispute Index shows, nearly three-quarters of cardholders consider disputing a charge to be a valid alternative to a refund. Rather, we need to strike a balance here. It’s important to offer a convenient and customisable experience, but not if it means that we fail to encourage responsible use of these tools and platforms.

Consumer education about proper use of banking apps, mobile wallets, and other digital payment and finance platforms should be a priority within the fintech space. Consumers need to be clear on what constitutes proper – as well as improper – use.

Going back to chargebacks as an example, users should be informed regarding what the dispute process entails, and the situations in which it’s acceptable to initiate a dispute. They should also be made aware that, even when they may have a valid reason to file a chargeback, that is not always the best approach. In some cases, they may see faster resolution by contacting the merchant, for instance.

We’re experiencing a generational transformation of the ways in which people think about payments and finance. We’re still just in the early stages of that transformation, though, and the approach we take in this phase will establish new norms going forward. We can’t afford to take this moment for granted.

Sponsored by Chargebacks911, the winner in the Tech of the Future – Chargebacks category at PayTech Awards 2023