State of play: GenAI in financial services

Each month, Philip Benton, Principal Fintech Analyst at Omdia, explores a new topic and assesses the “state of play”, providing an in-depth analysis and understanding of the market landscape.

This month, Philip takes an in-depth look at GenAI in financial services.

I’ve stayed away from writing a ‘state of play’ piece on generative artificial intelligence (GenAI) due to the sheer pace of change and my concern that any analytical take could quickly become obsolete.

However, the recent FinTech Futures AI Insights event was the ideal opportunity to take stock of the progress that has been made in the FS sector thus far, and with the end of 2023 fast approaching, now seems as good a time as any to (perhaps foolishly) predict where 2024 could take us next.

AI predates the Internet

First, it’s important to provide some historical context. GenAI is undoubtedly the hot topic of 2023, but it’s easy to forget that GenAI is not a new concept. Researchers and enterprises have tinkered with the idea of generative artificial intelligence – leveraging AI to “create something new” – for many years.

For example, natural language generation (NLG) is a GenAI concept that researchers have experimented with since 2015 (and the field has existed since the 1960s). AI has of course been around for far longer than GenAI, with the field of AI research being introduced in 1956, decades before the birth of the world wide web.

AI and particularly GenAI are poised to play an increasingly critical role in legacy modernisation efforts as organisations recognise its potential to drive innovation and digital transformation. Using AI-powered tools, financial institutions can transform their automation capabilities across fraud detection, sanction screening, credit assessments, customer service, and a multitude of other growing use cases.

AI has been spoken about for a long time in financial services and, according to Omdia’s IT Enterprise Insights 2024 survey, 93% of the banking industry are already looking to adopt AI in some form, with over half of the respondents having already implemented (or are currently implementing) AI within their organisation.

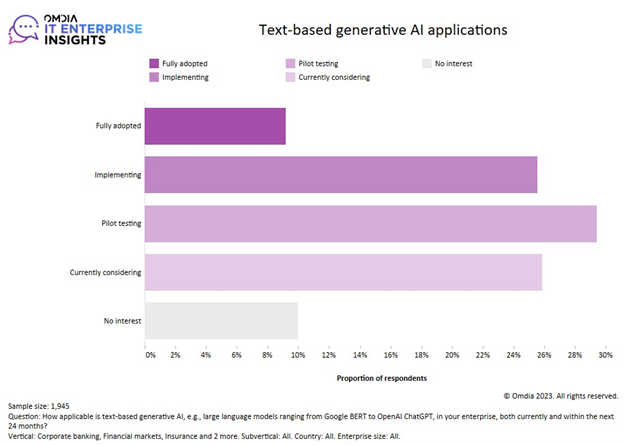

GenAI adoption is, naturally, behind traditional AI usage with the survey finding that just 9% of respondents in the financial services sector have fully adopted text-based generative AI applications within their institution. The majority (56%) of respondents are still in the experimental phase of GenAI and are either piloting or still considering how GenAI technology should be adopted.

GenAI is in the ‘experimental phase’ in the financial services industry. Source: Omdia IT Enterprise Insights Survey 2023/24

ChatGPT 4.0 is the “iPhone moment of the 2020s”, but it won’t necessarily dominate

The “ChatGPT reached x users in y days” slide must already be the most overused of all time, so much so that I loathe to see it in any presentation now, but it was certainly the catalyst for such rapid progress in 2023.

During the FinTech Futures AI Insights event, Michael Conway of IBM made the point that pre-ChatGPT 4.0, financial institution customers wanted to solve a business problem using technology, but now the mindset has shifted to “How can we use this tech to find a problem that needs solving?”

When Apple launched the iPhone in 2007, it wasn’t the first smartphone (the idea of mobile + internet was already made famous by BlackBerry), but it did spawn the era of ‘apps’, which fundamentally changed how banking and payments occur today. ChatGPT 4.0 has a similar feel, not least when OpenAI recently announced plans to launch its own GPT store, and although I don’t think the ‘killer’ use case has emerged yet, it won’t be long.

While ChatGPT is by far the most well-known large language model (LLM) chatbot, it is not five years ahead of its competitors (as Steve Jobs famously said when launching the iPhone at MacWorld 2007), and there’s a growing cohort of other LLMs which are all vying to quickly take market share. My colleague Andrew Brosnan explained in his keynote presentation at the FinTech Futures AI Insights event that ChatGPT does not define the GenAI space. “Frontier models like OpenAI’s ChatGPT are growing larger but make up the minority of GenAI deployments,” he said.

ChatGPT is in fact prohibited at many financial institutions, with the likes of Citigroup, Goldman Sachs, and JP Morgan having all banned employees from using the technology for bank business due to concerns of sharing confidential information on an open-source model. This has prompted many banks to consider creating their own LLMs to reduce the risk of data being compromised, as financial institutions rated ‘security’ and ‘privacy exposure’ as the biggest risks of AI within their organisation according to Omdia’s AI survey, ranking as a bigger concern than workforce displacement.

GenAI use cases dominated by internal scenarios, with external use cases to emerge in 2024

Omdia’s AI team has identified several near-term use cases for generative AI which apply directly to financial services, namely:

- Virtual assistants (for customer and employee interactions)

- Automated report generation (report writing and summarisation, copywriting, and blog posts)

- Search engines (returning specific information, synthesised from multiple sources)

- Software development (code modernisation, bug fixing, and predictive coding)

Presently, the majority of ‘active’ use cases are internal facing. GenAI is being used to improve processes and operations to assist employees, sometimes for external customer queries, but adoption is kept internal for now. Google’s Narinder Patti stated during a panel at the FinTech Futures AI Insights event that many of their existing use cases are around extracting and summarising data and documentation, saying: “We focus on low risk, high productivity gains.”

Morgan Stanley, for example, deployed OpenAI and trained GPT-4 on its vast back catalogue of wealth management content to allow their employees to query the internal chatbot and obtain instant feedback on the correct advice or insight to share with their clients.

In 2024, the obvious external use cases for GenAI will be revamped virtual assistants. Banks have been big advocates of chatbots to lessen the load on their contact centres and to ensure their staff focus on more complex queries. Bank of America’s Erica chatbot has surpassed 1.5 billion interactions since its 2018 launch and its customers engage 56 million times per month.

However, most chatbots are not ‘intelligent’ in their ability to assimilate information, often requiring humans to step in, whereas GenAI chatbots should be able to handle 90% of day-to-day queries end-to-end. There remains the risk of hallucinations, but there are other emerging technologies that are helping to mitigate hallucinations and strengthen accuracy, such as retrieval augmented generation (RAG).

Financial services remains one of the most highly regulated sectors, and with AI legislation on the horizon, I’m anticipating a lot of the innovation in 2024 will focus less on new revenue-generating business models and more on helping existing initiatives realise operational efficiencies, such as automated approvals for dynamic loans.

Also, cybersecurity and anti-fraud is an increasing use case focus, with GenAI likely to lead to an unprecedented rise in scams, including deepfakes, automated phishing, and malware creation.

The financial services sector is traditionally cautious when it comes to the adoption of new technologies due to regulatory, safety, ethical, and legal concerns, and while there is a lot of excitement around the potential of GenAI and the speed of innovation, I think the idea of GenAI being the default interaction engine for a customer when engaging with a bank is still a long way off.

About the author

Philip Benton is a Principal Fintech Analyst at Omdia and writes analysis on the issues driving technological change in financial services. Prior to Omdia, he led consumer trends research in retail and payments at strategic market research firm Euromonitor.

Philip Benton is a Principal Fintech Analyst at Omdia and writes analysis on the issues driving technological change in financial services. Prior to Omdia, he led consumer trends research in retail and payments at strategic market research firm Euromonitor.

In this column, Philip will discuss the technological implications and consumer expectations of the latest fintech trends.

You can find more of Philip’s views on fintech via LinkedIn or follow him on Twitter @bentonfintech.