Acquiring pricing models

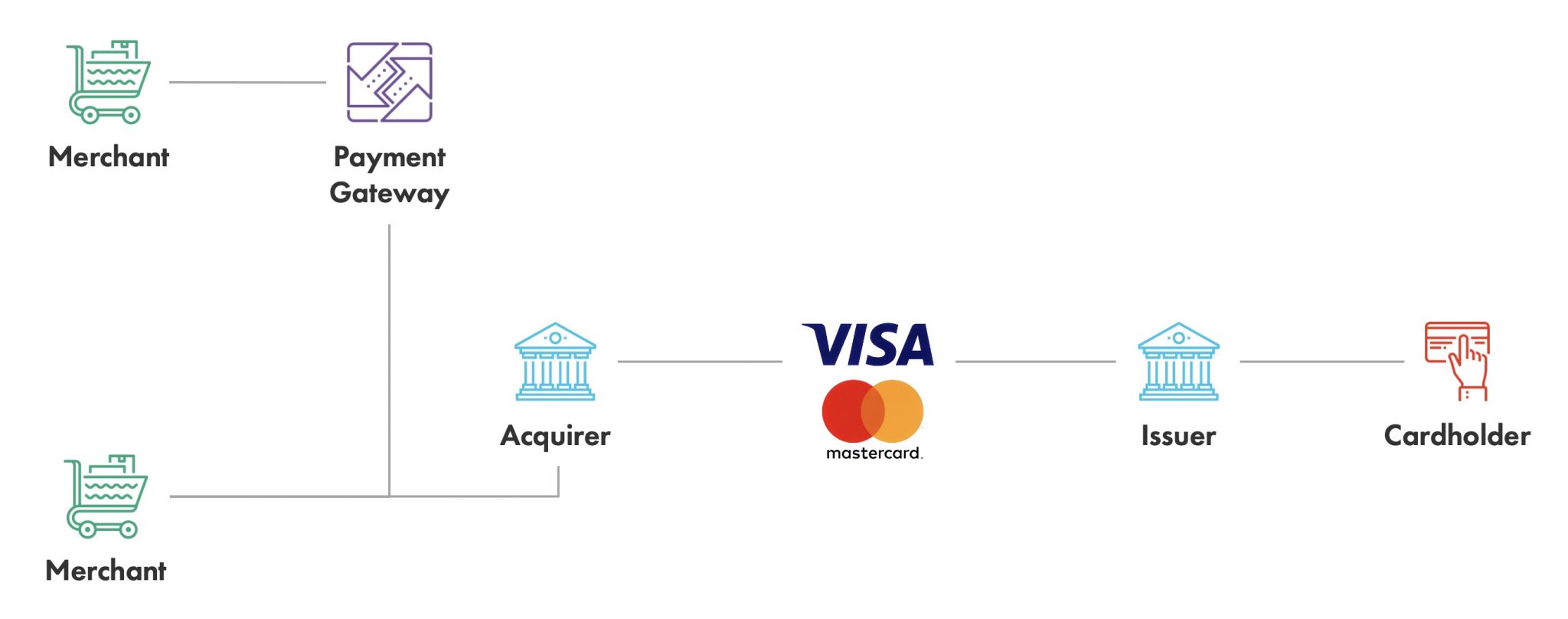

The payments world brings together issuers, cardholders, acquirers, payment gateways, facilitators, merchants, processing centers, and payment vendors with the payments company (Mastercard, Visa, etc) playing the most important role in transaction management and processing, as well as in the financial relationships between all parties.

Source: DataArt

In addition, the payment company supports further cooperation between the acquirer and issuer sides, and regulates equitable distribution of fees from transactions. Typically, issuers don’t charge cardholders a per transaction fee, but acquirers are paid transaction fees by merchants/payment facilitators. Payment models allocate fees between acquirers and issuers, charging an interchange fee for every transaction from the acquirer and sharing this fee with the issuer. Therefore, the issuer can generate revenue from transaction processing and does not need to levy a fee on cardholders.

The amount of the interchange fee depends on many transaction parameters. The number of transaction parameters is contingent on the particular payment company (Mastercard, Visa) but we can highlight common parameters for all, and divide them in groups:

- Transaction properties: amount, transaction conditions, transaction region;

- Card properties: card product, i.e. Visa Gold/Mastercard purchasing, account funding source (AFS) (debit/credit/prepaid), chip/contactless/virtual;

- Device properties: (card and cardholder capabilities, card present/not present, merchant category code).

As a result, there are many rules applied in calculating the interchange fee and they are derived from the possible combinations of parameters plus any other specific characteristics or conditions.

European acquirers are required to show their merchants statements detailing the fees charged, including the interchange fee. Therefore, acquirers must calculate the interchange fee on their side. They have two options:

- Charge merchants higher fixed rates to cover all possible interchange fees.

- Calculate interchange fees based on the rules provided by the payment model.

Source: DataArt

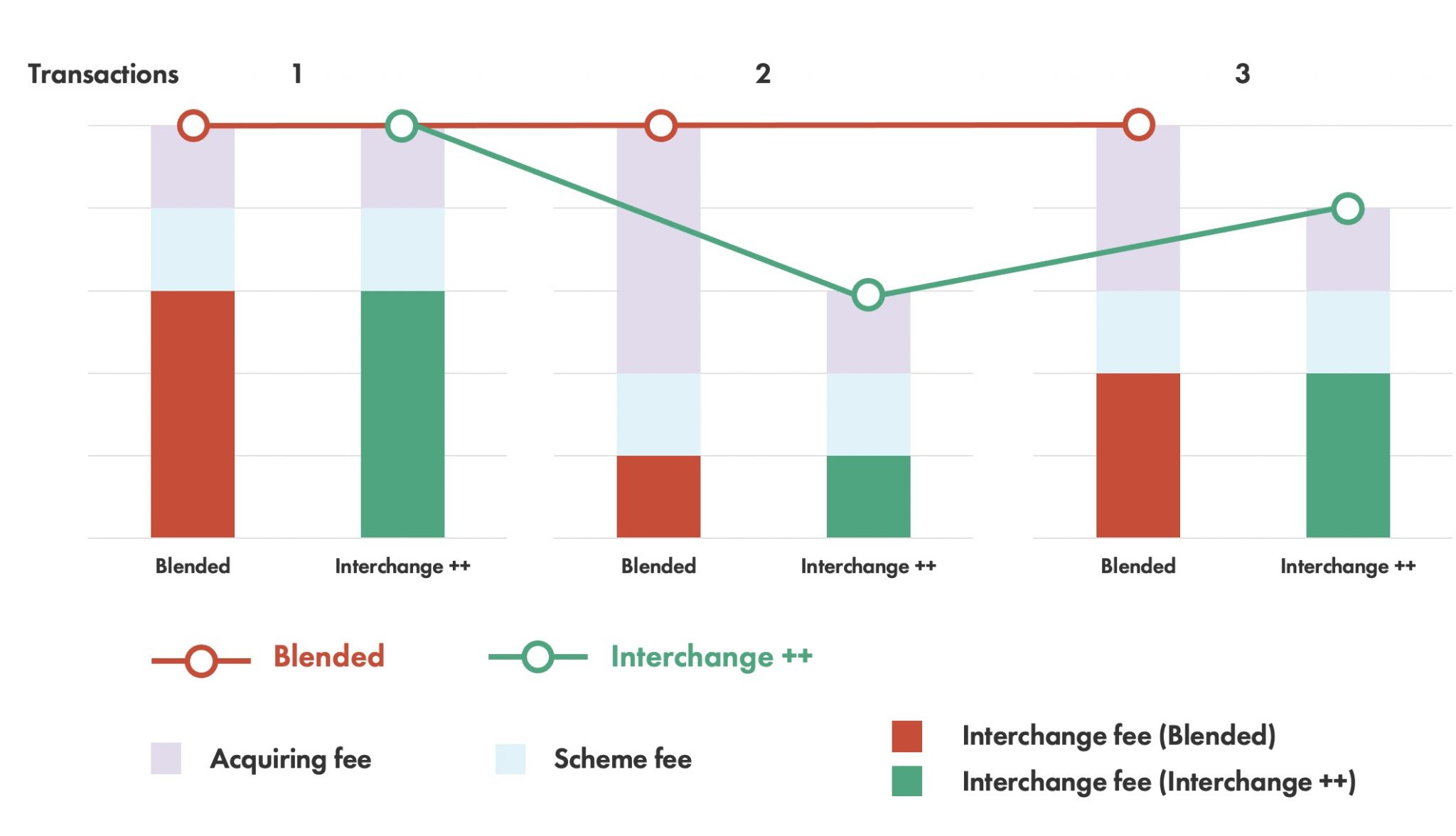

Acquirers can choose between two options related to merchant pricing models – blended and interchange ++.

Both pricing models include interchange fee rate and scheme fee rate required by the payment system and acquiring fee that includes the acquiring bank margin.

Merchant Fee = Interchange Fee + Scheme Fee + Acquiring Fee

But the principal difference in these pricing models is the interchange fee value calculation.

We have noted that the interchange fee depends on the transaction properties. In the blended pricing model, the interchange fee may be predicted as a fixed value using payment interchange rates and the usual transaction scope for the existing merchants.

For example, transaction scope can be divided by the region (domestic/intraregional/interregional) and transactions conditions (card present/card not present). So, in a blended pricing model, the interchange fee values might be limited by maximum or average available rate in the payment systems interchange fee specifications – depending on the transaction properties (card present/not present and the region) or any other groups relevant for the particular acquirer.

Acquirers who use the interchange ++ pricing model calculate the interchange transaction fee based on the payment systems requirements on the acquiring side. The acquiring processing platform may support a new module of interchange fee calculation or may have a separate system that pre-calculates the same fee as the payment system. Merchants using the interchange ++ pricing model are charged an accurate pre-calculated fee. Such models are more attractive for merchants because they receive clear transaction statements with detailed information about the interchange fee paid to the payment system.

Let’s summarise the benefits and challenges presented by each merchant pricing model below:

| Blended pricing model | Interchange++ pricing model |

| Challenges | |

| Monitors changes in interchange fee rates and updates blended rates accordingly | Must prepare acquiring platform and develop or buy a separate system to pre-calculate accurate interchange fees |

| New transaction scope makes it necessary to rebuild prices | Support new requirements for interchange fee calculation from payment system on bi-annual releases |

| Benefits | |

| The technical solution for charging fees is not changed | Accurate fee calculation maximises profit |

| Attractive to merchants | |

| Settlement files are sent by close of business, and there is no wait for the payment system to calculate the interchange fee | |

The interchange + pricing model is the most competitive model for acquirers who value their merchants and other third-parties such as payment gateways, payment facilitators and wish to offer attractive service options.