Retail banks ignore social media data at their peril

Jean Pierre Kloppers, BrandsEye: social media is a largely untapped source of data for the banks

In the UK, new digitally-focused challenger banks are emerging as serious contenders to the established high street banks that have dominated the retail market. With mobile customer-centric products and easy onboarding, these new players are gaining customers and in turn, drawing significant volumes of consumer conversation on social media.

This online conversation has typically been considered the realm of marketing and PR. However, when analysing the data at scale by structuring it for sentiment and the specific issues driving that sentiment, new operational and strategic opportunities for the entire industry emerge.

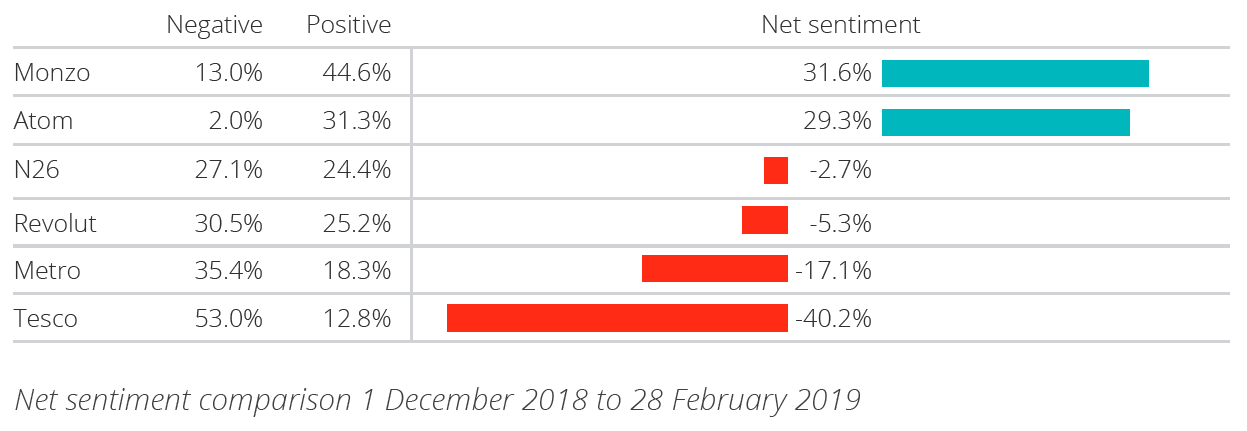

BrandsEye’s analysis of 118,460 tweets about six UK challenger banks from December 2018 to February 2019, suggests that social media is a valuable and largely untapped source of data for the banks. From concerns on governance to crucial customer experience feedback, it presents opportunities for both incumbents and new entrants.

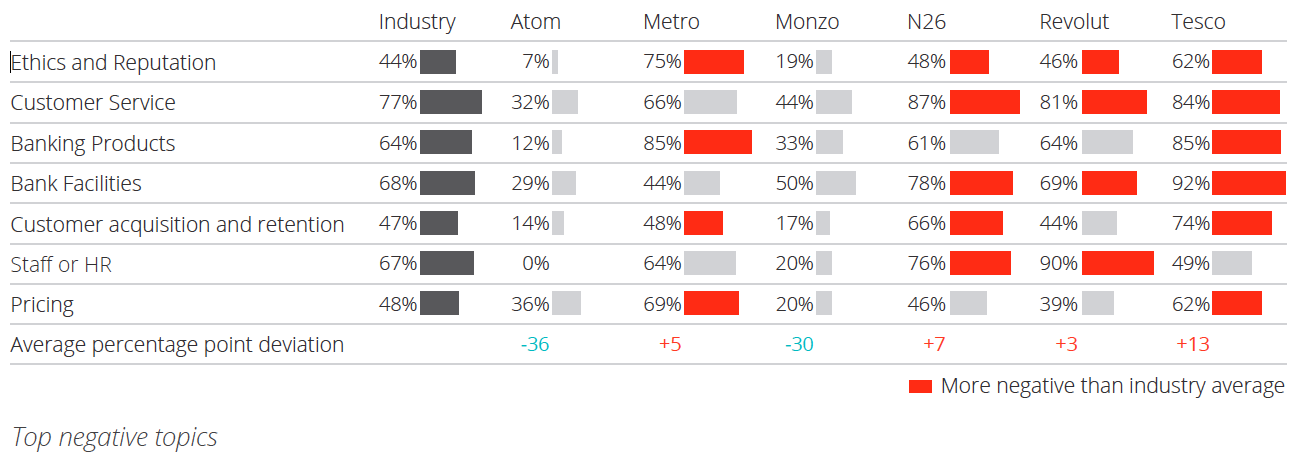

Digital innovation, particularly around app functionality, is a key differentiator for the new entrants. 23.4% of consumers who recommended a challenger bank did so based on their positive experience with the bank’s app. Monzo’s app, in particular, drew positive sentiment. Metro Bank’s decision to invest in physical branches seems to be paying off as 24% of consumers recommending Metro Bank cited their branch experience.

Challenger banks also appear to be more adept at customer query resolution. Lengthy processes and digital downtime for incumbents are driving their customers to consider moving to challengers.

Today it is becoming increasingly difficult for banks to differentiate on price or product, and so the battle for customers will be won or lost on customer experience. According to the McKinsey 2019 report, “Rewriting the rules: Succeeding in the new retail banking landscape”, customer experience is a key battleground for growth and building loyalty for retail banks. The report notes that retail banks have not kept up with customer experience improvements seen across other industries, instead opting to invest in brand building to bolster reputation and stave off competition. A reputable brand, McKinsey argues, once stood for “trust and security and became a moat providing protection against new entrants to the sector”. But the opposite is now true and banks must look for new ways to make customer experience gains.

To do this, they cannot afford to ignore social media as a source of volunteered customer experience data. Traditional customer and market research methods and tools, such as Net Promoter Score (NPS) surveys and focus groups, provide useful review data but are backwards-looking indicators. They cannot provide an immediate understanding of the customer experience. Social media provides a real-time stream of customer opinion across a whole market, without anyone prompting or guiding customers on what to say or how to say it. Understanding this accurately, comparatively, and in real time is a significant competitive advantage.

Typically, organisations measuring consumer opinion on social media would get skewed results as PR, press and marketing efforts are combined with operational customer experience insights. Separating this data will be key for banks to take learnings from online feedback to make actionable improvements to channels and stages on the customer journey.

As consumer demand for personalised and always-on banking grows, digitally astute challenger banks are well positioned to capture market share from their high street competitors. Long processes, slower on-boarding and fewer digital channels of engagement will propel more consumers to consider taking up accounts with the challengers.

While the legacy plumbing of high street banks’ IT infrastructure and the “moats” they’ve created over time may yield a slower pace of digital transformation, the challenger banks cannot afford to rest on their laurels. Our research found that Monzo and Atom Bank were the only banks who received more praise than complaints. They were the only banks where turnaround time complaints comprised less than 10% of emotive conversations.

Challengers are likely to face signific competition from fintech start-ups, and from the established high street competitors. RBS has already created Bó, an online-only bank to rival the likes of Monzo, that according to the Financial Times, will “take on the digital challengers at their own game”. Santander has announced that it would be expanding its branchless Openbank from Spain to other countries.

The future of banking will be increasingly digital and personalised. In order to deliver on customer-centric products and services, that have stood the challenger banks in good stead, all banks must keep their finger on the pulse of customer sentiment to make continuous improvements.

By Jean Pierre Kloppers, group chief executive, BrandsEye