Open banking, PSD2, and the urgent need for banks to “think different”

On Saturday the EU’s second payment services directive (PSD2) came into force across most of the continent, forcing banks and payment companies to share data with third parties (if their customers agree).

(As a customer of NatWest Bank for over 25 years I’ll certainly agree. In all that time I don’t remember the bank offering me anything of interest beyond a few core banking services. Perhaps more dynamic organisations will use my data to create new and attractive offerings for me…)

The aim of PSD2, or “open banking” in the UK, is to increase competition between banks and stimulate the creation of new value for customers. As things currently stand we are likely to see banks lose out significantly. Non-banking companies with platform-based business models will capture most of the value.

Indeed, many in the industry believe that up to 50% of European banks profits are at risk over the next five years, with fundamental macro-economic trends compounding changes like PSD2.

With Price-to-Book ratios at record lows, and slow or no revenue growth, it’s clearly time for those running banks to think much more boldly and much more creatively about how they transform for this new world. So far most banks (like most incumbents in most industries) have been tinkering: digitising their existing operations, integrating with some fintechs, creating new technical capabilities like APIs, but not whole-heartedly committing to bold transformation of the fundamental business model.

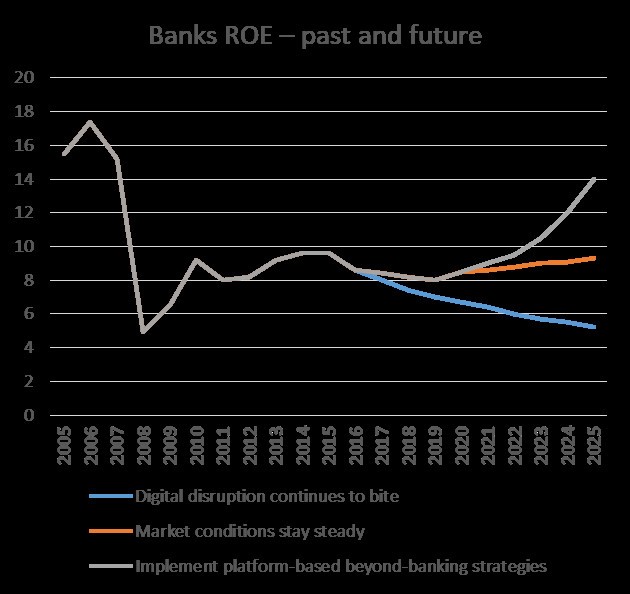

McKinsey, in its recent “Remaking the Bank” report, charted three possible futures, summed up in the chart across, which I’ve adapted (“ROE” is net income divided by bank capital, a key measure of banking performance). The blue line puts the banks into financial crisis territory again.

A bright future with meaningful growth potential requires the adoption of a platform-based “beyond banking” strategy. The challenge today is, as in most incumbent sectors, that there is very little understanding of what this means in practice or how to implement it.

It requires quite a fundamental re-think about the way a bank creates, shares and captures value in a hyperconnected world. Orchestrating – at scale – a carefully curated ecosystem of producers and consumers of value adding solutions (banking and non-banking) is the key.

Banks already have enviable assets which they can leverage – large, loyal customer bases, deep local market knowledge, huge amounts of data, trusted brands, government support, strong balance sheets and technical expertise.

Below is a tremendous video that helps bring the opportunity to life, that all banking execs should watch.

It’s by the chief digital officer at Deutsche Bank, presented at MIT’s Platform Strategy Summit in Boston earlier this year. He and his team took the time to fully understand how advanced business models work, and then found a way to start to integrate them within the bank’s existing operations, as part of a new digital transformation strategy.

But even once the rationale is explained in this way and leaders can see these business models in operation, the challenge of driving a transformation at scale in a way that moves the needle is significant.

Boards and executives are still driven by traditional banking metrics and existing ways of thinking about the world which mitigate against investing effectively in corporate renewal.

I’ve found that to get stronger executive attention we need to put the strategic opportunity in language that boards and execs understand: hard numbers showing a) the potential impact in particular on valuation and b) the level of capital and resources that need to be re-allocated as part of a new business model portfolio approach.

Here’s an example I did for a bank recently, bringing to life the tiny proportion of capital and resources that are currently being allocated to new business models and the impact that was having on growth and value:

It can be taken further to show the potential impact on valuation of evolving the business model portfolio in this way over time (with this example there was a $150 billion potential uplift with new business portfolio) . The analysis can be supported by new artificial intelligence (AI) tools that remove biases as well as providing automated benchmarks of how other companies (typically in other sectors) have made shifts in business model mix over time and the impact on their valuation.

The debate with the board is then about whether the potential uplift in market value is $150 billion or “just” $50 billion. Either way, we now have the attention of the leaders and the notion of true business model transformation becomes a strategic priority.

What’s then needed is a “playbook“, a practical guide for the organisation on how to move forward to realise the $50-150 billion opportunity. That’s what I help create.

Large banks grew in the past into important organisations by aggregating multiple services into a portfolio of offerings. In a digital world this approach can be dramatically extended, by going beyond banking and applying the principles of platform-powered network orchestration.

With PSD2 now in play it’s time for banks to radically re-allocate capital to this new approach. Digital hybrid companies, like Amazon and Alibaba, are not sitting still. Banks have all the technical assets needed to create, share and capture value in a new more exciting way. The key, in the words of Steve Jobs, is to “think different”.

By Simon Torrance

Simon Torrance is a senior independent advisor to boards and leadership teams around the world, specialising in business model transformation and platform strategy. He has been a member of the World Economic Forum’s global agenda council and has an MA from Cambridge University.

Based on brand new research on financial performance of hundreds of businesses, Simon has designed and created a brand new learning and consultancy programme for senior executives: The New Growth Playbook.