Fintech companies will be a new kind of business in 2018

Ben Jackson, NBPCA

Fintech companies will find that they are a different kind of business in 2018 than they were in 2017, writes Ben Jackson, COO of Network Branded Prepaid Card Association (NBPCA).

The final rule for prepaid accounts from the Consumer Financial Protection Bureau (CFPB) applies the same rules to many payment companies that govern traditional prepaid providers, even ones who never thought of themselves as being in the prepaid business.

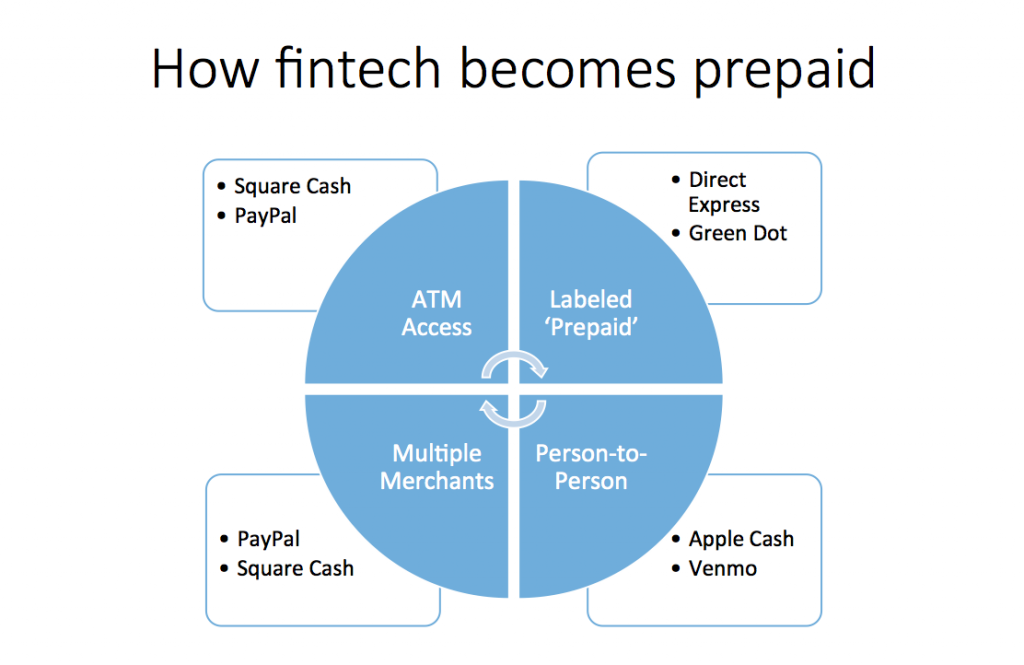

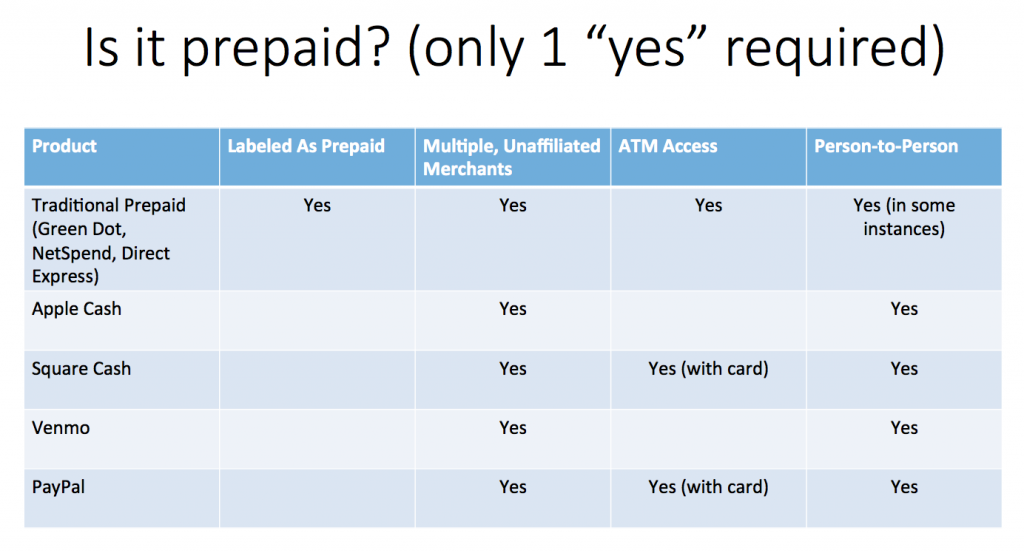

The 1,687-page rule defines a prepaid account as one that is “issued on a prepaid basis or capable of being loaded with funds, whose primary function is to conduct transactions with multiple, unaffiliated merchants for goods or services, or at ATMs, or to conduct person-to-person (P2P) transfers, and that are not checking accounts, share draft accounts, or negotiable order of withdrawal (NOW) accounts”.

So, if a company is storing money, but not opening a bank account for its customers, they are in essence offering a prepaid device. That means many fintech companies and other businesses will need to make sure they have processes for delivering new kinds of disclosures, identifying their customers, and managing dispute resolution, among other tasks.

These are things that many companies have never contemplated because they have never considered their products as prepaid, and really, neither have their customers. However, none of that matters to CFPB. As all law enforcement is fond of saying – ignorance of the law is no excuse.

A variety of industry analysts have observed that many fintech companies will find themselves having to comply with these new rules. Companies such as Apple, Google, PayPal, Samsung, Square and Venmo need to adjust the way they bring customers on board and manage accounts of current customers.

These companies will need to figure out how to take a simple mobile signup process into the world of prepaid card compliance with multiple layers of disclosures (a short form, a long form, and terms & conditions). For companies like PayPal, complying with the rule may be more manageable because they have in house experience with prepaid products.

Other companies likely will need to look to the prepaid industry for best practices and examples of how to bring clients on board through different channels. They do not need to reinvent the wheel, since prepaid companies have been doing this for a long time and preparing for the new compliance regime.

While certain companies clearly will fall under the rules, there are others who may end up in a gray area. Nonetheless, any companies with products that facilitate payments without credit or debit cards will want to look closely at the rules and be prepared to update their compliance plans.

The payments industry has relied on prepaid accounts for every innovation, whether it is mobile payments, wearables, or the internet of things (IoT). As innovators develop the next new thing, they should partner with the prepaid industry to ensure their progress does not get entangled in a compliance web.