ECB Guide: assessments of fintech credit institution licence applications

New fintech licensing guide from ECB

The European Central Bank (ECB) has published a guide to assessments of fintech credit institution licence applications.

“As a result of technological innovation in the banking sector, a growing number of entities with fintech business models are entering the financial market,” states the ECB. “This is mirrored by the increasing number of credit institution licence applications submitted for authorisation to the ECB by such entities.”

The guide refers to “bank business models in which the production and delivery of banking products and services are based on technology-enabled innovation”, the ECB explains.

“The ECB aims to allow scope for innovative market participants to contribute positively to the financial sector and seeks to achieve this, in accordance with its mandate to maintain the safety and soundness of the European banking system, by maintaining adequate prudential standards for newly licensed banks.

“ECB policies that apply to the licensing of any bank within the Single Supervisory Mechanism (SSM), as presented in the Guide to assessments of licence applications, also apply to the licensing of fintech banks. The ECB’s role is to ensure that fintech banks are properly authorised and have in place risk control frameworks for anticipating, understanding and responding to the risks arising in their field of operations. Equally, to ensure a level playing field, fintech banks must be held to the same standards as other banks,” the ECB states.

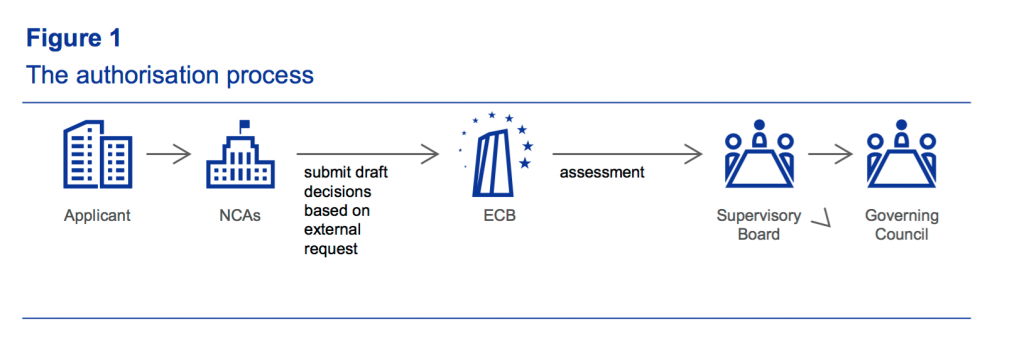

Source: Guide to assessments of fintech credit institution licence applications, ECB

“The purpose of this guide is to enhance transparency for potential fintech bank applicants and increase their understanding of the procedure and criteria applied by the ECB in its assessment of licence applications. This transparency is also intended to facilitate the application process. In this context, the guide is technology-neutral and seeks to neither support nor discourage the entrance of fintech banks as market participants, compared with banks with other types of business model.”

Click here to read the full guide published by ECB (PDF format)