The Monday mindset: 30 January 2017

Fintech zeitgeist! Welcome to the third in a new series of brief reports. Every Monday, we might look back at last week; look ahead to this week; share a few thoughts (our own or others); or discuss anything that catches our eye. This week we welcome the views of guest writer Soumik Roy.

Last week, Deutsche Bundesbank hosted the G20 conference “Digitising finance, financial inclusion and financial literacy” at the Biebrich Palace in Hesse, Germany. Speaking at the conference, G20 members and representatives of prominent fintech hubs such as Hong Kong and Singapore, discussed how the industry could reveal how to realise the benefits of digitisation while simultaneously mitigating the risks it involves.

Welcoming a roomful of bankers to the conference, Dr Jens Weidmann, president of the Deutsche Bundesbank quoted business magnate Bill Gates who once said “Banking is necessary, banks are not” – and Weidmann had everyone’s attention at once.

In his address, Weidermann talked about the potential of technology to revolutionise financial services by driving efficiency gains, increasing competition, and facilitating access to financial services. He also talked about the promise of blockchain, big data and analytics, and how they have forced central banks to step out of their comfort zone to experiment and understand them better.

While there are many risks associated with tech-based financial products and solutions, Weidermann advises central bankers to be cautious as fintech business models have not yet run through an entire credit cycle and their experience with digital finance in economic downturns is very limited. Further, he suggests that the industry be regulated “smartly” so as to avoid hindering the growth of fintech start-ups. The Deutsche Bundesbank president also mentioned that the German G20 presidency will take stock of the different regulatory approaches and develop a set of common criteria for the regulatory treatment of fintechs.

From the looks of it, Widermann has faith in fintech solutions and is gearing up to make a mark on digital finance during Germany’s G20’s presidency, which ends in November this year. Incidentally, shaping digitisation is also on his list of priorities for discussions between finance ministers and central bank governors and among the G20 working groups.

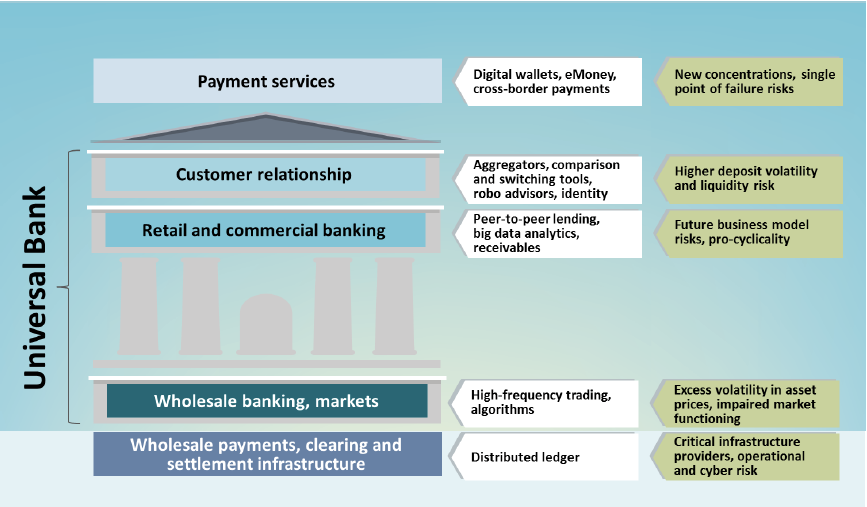

Dr Mark Carney, governor of the Bank of England and chair of the Financial Stability Board also made an interesting speech at the conference. He shares a story from his adolescent years about working as a teller in a bank in Canada, and his experience with regular clients as a frontline executive. Through this example, he introduced the financial services value chain, the fintech solutions that impact the different segments of the value chain, and the risks arising from this transition.

Financial Services Value Chain with Potential Issues for Financial Stability

The disruptions and risks faced by the components of the financial services value chain are:

- Payment services, which are being disrupted by digital wallets and electronic cross border payments increase concentration and single point of failure risks.

- Customer relationship management, which are being replaced by robo advisors and aggregators who seem to be better able to assist customers, increase deposit volatility and concentration risk.

- Retail and commercial banking customers are now turning to P2P lending services and big data analytics but are increasing future business risks and pro-cyclicality which could further amplify the impact of economic and financial fluctuations to their business.

- Wholesale banks are being coupled with high-frequency trading and algorithmic trading to increase returns but this impairs market functioning and makes asset pricing extremely volatile.

- Wholesale payments, clearing and settlement infrastructure are all being disrupted by blockchain, many of whose prototypes are being tested by central banks in Germany, the UK and India. However, the regulators need to recognise that it increases their dependence on critical infrastructure providers and increases operational and cyber risks.

From his speech, it is evident that Carney is actively thinking about fintech and investing resources in getting more out of the technology, faster. Back home, he has a regulatory sandbox, a fintech accelerator, developing proof of concept applications that leverage cutting edge new technology, and is expanding access to central bank money to non-bank payments service providers – and he suggests everyone else do the same if feasible.

In my opinion, in the near term, we’ll see a whole load of blockchain applications taking over the financial services industry, whereas in the medium to long term, we’ll have a second wave of disruption led by artificial intelligence (AI).

Here’s why: for a tech-based solution to be successful, it needs to be accepted and adopted by people. Since much of blockchain powered applications are backend systems, roll-outs will be smoother, uptakes will be easier, and companies who purchase these solutions will see immediate benefits.

For AI-powered solutions, the time for mass adoption is yet to come, but I’m confident that five years from now, people will prefer dealing with robo-advisors to manage their banking transactions, manage their savings, investment and pension goals, and even discuss legal-jargon about loans and mortgages.