Who will win the battle for millennials – Zelle or Venmo?

Neil O’Brien: Will Zelle be a genuine innovator or just a clearXchange rebrand? And what will it offer that Venmo doesn’t?

As a Gen Xer, I have always had difficulty relating to the obsessive appeal social media has to millennials. Tweeting and Facebook posting of mundane daily events seemed like over-sharing and just a little narcissistic to me. This is not an intellectual problem of understanding the concepts or technologies, but a kind of generational disparity of views about what is appropriate to communicate socially. I accepted this difference long ago and didn’t pay it more attention.

Then one day it popped up in my work. A P2P payments startup called Venmo was quickly becoming hugely popular with millennials. I took a look. The payments technology was nothing really new. What was surprising was the social media aspect – lists of who paid whom, and for what, and how many minutes and seconds ago. I was surprised this was here at all. I was more surprised it was all over the front page. Isn’t payments just about moving money from A to B as fast, securely and cheaply as possible? What does social media have to do with payments anyway?

Clearly, there was something more going on than moving money around an electronic payments network. I began to understand by asking the right question: what human needs are addressed here?

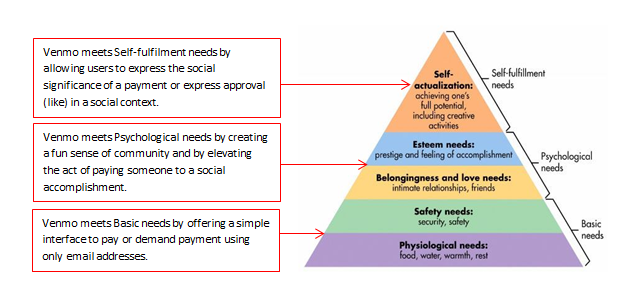

One of the most well known frameworks for thinking about human needs is Maslow’s hierarchy. This framework, in its original form, orders needs from basic (deficiency) needs, through psychological needs to self-fulfilment needs.

The value of Maslow’s framework in a business context is not in prescribing the order in which needs should be met (it doesn’t), but in providing a way to think about the relative potency of a product or service that meets a higher order need versus a lower order need.

How Venmo meets human needs at multiple levels

Take a look at how Venmo meets human needs through the lens of Maslow’s needs hierarchy.

Venmo addresses needs at different levels in Maslow’s hierarchy at the same time. It meets the basic need to pay someone or demand payment from someone. This is a basic financial survival – the financial equivalent of food/water/shelter. It does this with a level of security that has some inadequacies, but these are clearly not enough to override the value it provides by meeting higher order needs.

Venmo addresses psychological needs by creating a fun community where people want to go and see what their friends are up to, as reflected in their payments to friends. The public display of each payment (stripped of the amount) proclaims a small accomplishment, an act that contributes to belonging to a community.

Finally, Venmo addresses a form of self-actualisation that is ubiquitous in a world of people obsessed with social media, namely self-image actualisation. Contributing to this self-image actualisation is not only the social advertising that the payment itself was made but also the often witty or jibing comments that accompany the payment.

More generally, what Venmo has shown is the potential for a digital product to ascend the hierarchy of needs and provide value at multiple levels. The value provided at the higher levels not only makes Venmo a more compelling and attractive product, it also makes it more difficult to switch to an alternative because of the network effects embedded in the social aspect of payment.

Why does this matter?

Now, a collection of America’s biggest banks has unveiled a new name for their Venmo-killer: Zelle.

Zelle the Venmo-killer. Sets the expectation nicely.

Venmo processed $7.5 billion in payments last year. Some large banks processed more (Chase QuickPay processed $16 billion last year), but the Venmo growth rate is impressive – 175% increase over prior year. And importantly, this growth rate is in the millennial demographic. Banks see a threat.

What is at stake here is not just where millennials make payments, but where their minds are engaged in an activity related to banking. Millennials will go on Venmo just to see what is happening amongst their friends – even when they do not plan to make a payment. Who does that with a banking app from a traditional bank?

There isn’t any direct revenue loss to banks from Venmo, as P2P payments are generally free no matter who provides them. The concern is over what comes next. Will millennials find alternatives for other banking activities? Will Venmo now target fee-based services with an established customer base? Will banks just become pipes with no ownership of the customer relationship? This is a battle for the banking relationship with millennials.

Can Zelle succeed?

So, what are the chances Zelle will succeed? First of all, let’s define success here. The underlying payments platform – clearXchange – is already successful. It is used by millions of customers at major banks. So, more adoption of the same payments platform by the same customer demographic is not the definition of success.

Success for Zelle means displacing Venmo as the payment platform of choice for millennials. What are the chances of this happening?

Well, can you imagine a millennial who uses Venmo going back to a payment mechanism that is fast, secure, reliable and free, but doesn’t have the social dimension that is so powerful? That might be tough to give up. Even in exchange for a payment service that meets basic needs better than Venmo.

So, what exactly is a Venmo-killer going to do differently? Be more secure? Adoption of Venmo has never been impacted by industry questions about its security. Speed? Venmo payments are really next-day payments, even though they may look like same-day.

While most clearXchange payments are one to two days, some are same-day depending on the pair of banks involved. We can expect more focus on same-day or real-time payments from clearXchange. Although a new function, such as bill/cheque splitting could be included in Zelle, I’m expecting speed and security differentiators to be marketed as Zelle’s competitive advantages.

In summary, something better at meeting basic needs.

New name or new value?

But, meeting basic needs better and faster isn’t going to win the game. Because the game has already been changed from meeting basic needs to meeting higher order needs.

My bet is that Venmo can only be displaced by a new concept that meets higher order needs in a clearly superior or completely different way. In fact, the greater threat to Venmo may be competing offerings based on social networks, e.g. Facebook Messenger.

Will Zelle deliver new value? If Zelle is simply a re-marketing of clearXchange then the answer is pretty obvious. If Zelle is truly an innovation that provides compelling new value to millennials, then there is a fighting chance. Come October when Zelle is launched we will know the answer.

But until then, as we wait, we can marvel at the astonishing reality: the incumbent large bank payment offering clearXchange (and may as well include The Clearing House in that category) has now effectively become a “me too” offering playing catch-up to a company that didn’t exist seven years ago. Now that is true fintech disruption!

Broader implications

The contest between Venmo and Zelle has broad implications for the digital strategy of every financial institution that targets millennial consumers.

The outcome will show the world if banks really understand the millennial mindset. We will see if the combined efforts of multiple large banks can out-innovate a lone fintech disrupter.

If Zelle fails, traditional financial institutions will need to rely more on outward looking strategies to attract millennials – perhaps acquisition of focused fintech players or partnerships within social networks.

This contest is redrawing the boundaries of innovation in banking. Innovations amounting to better technology and friendlier user interfaces are necessary but not sufficient to attract millennials. The really successful innovations in consumer banking will move beyond basic needs and address the higher order needs of the target demographic.

By Neil O’Brien, former SVP, director of digital banking at Santander US