Tech-powered non-banks taking over US Treasury trading

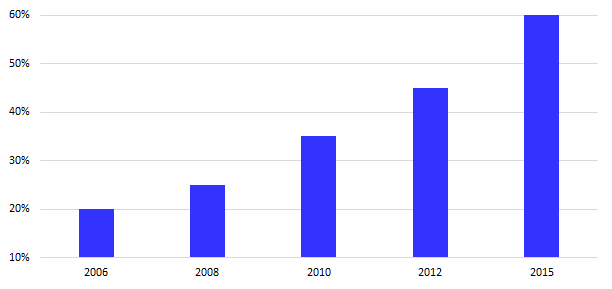

Non-Bank Interdealer Volume Market Share (Estimate) Source: Tabb Group

Technology is equipping non-bank market-makers to move into the US Treasury Market, giving them analytics and speed to manage and hedge risk, while enhancing market liquidity.

“Market makers have been deploying electronic tools at varying degrees over the past decade,” says Anthony Perrotta, a principal and head of fixed income research at Tabb Group, author of Metamorphic Market: Transformation in US Treasury Trading, which examines growth of the US Treasury Market, reduction of primary dealer balance sheets, emergence of non-bank market-makers and the evolving interdealer US Treasury Market trading ecosystem.

But Perrotta adds, “electronic adoption has accelerated recently and non-bank market-makers have increased their share of the liquidity provided to other market-makers and the broader market – as much as 60% of all on-the-run interdealer limit-order-book executed volume.”

A “bevy of catalysts are converging to instigate microstructure transformation”, delivering fundamental change to the fabric of the US Treasury market, which now stands at $12.6 trillion, a 180% meteoric rise from 2008.

Among other factors, new regulation is making it increasingly difficult for primary dealers to operate in capital intensive market-making businesses, evidenced by a significant reduction in a balance sheet committed to secondary market-making and inventories.

This rise of electronic interdealer liquidity pools has led to expanded use of technology-driven trading and automated decision-making to price, deliver and receive liquidity at increasing velocity. “The speed at which these emerging non-bank market-makers operate has shot from milliseconds to microseconds,” Perrotta says, sharing a note of caution, that although HFT has become a catch-all term in the lexicon for technology-driven firms, this misrepresents the differentiation that exists among non-bank firms providing liquidity in US Treasury markets.

As market and liquidity risks become more ambiguous, US Treasury market participants have gravitated towards a hybrid ecosystem combining the characteristics of modernisation with the use of disclosed relationships, producing a symbiotic paradigm. According to Perrotta, “We’re also seeing market-makers building disclosed, direct-trading relationships to complement trading activities in anonymous, limit-order-book pools, providing them with more options than in the past to manage and hedge US Treasury risk.”

This new paradigm is in its infancy, Perrotta says. ”Traditional behaviours need to be augmented and new market-makers have to secure the trust of incumbents. In a world of relationships, worth is defined by how well they stand up when tested.”