The Future of Payments: towards a vision for 2020

Daniel Szmukler is a director at the Euro Banking Association.

While the payments landscape has evolved rapidly over the past decade, due to a flurry of innovation and regulation, expansive growth in electronic payments and the inclusion of new market entrants, industry research1 indicates that the next decade will yield a period of even faster changes, writes Daniel Szmukler, director, Euro Banking Association.

In the traditional electronic payments sector the weak global economy continues to drive cost efficiencies in both domestic and international payments systems. International trade expansion and globalisation are growing the demands for euro-denominated payments and the rapidly changing demands of corporates, non-banks and banks for lower, reduced fees and improved services will increase pressure on traditional payments models to rationalise.

The retail payments sector is already undergoing major change primarily as a result of the disruptive impact of e-commerce mobile and tablets. There is a rapid development of new payment concepts and business structures which will displace traditional cash and other forms of payments. Consumers, banks, merchants and regulators are having to realign their visions and rethink commercial models.

Recognising these trends, in 2012 the Euro Banking Association embarked on a comprehensive exercise to develop a long-term vision for payments that should ensure that the EBA value proposition continues to serve the needs of its diverse membership and their end customers. The development of this vision was driven in large part by research2 and a brainstorming workshop that engaged EBA Board members to re-assess the changing needs of the payments industry.

The future promises to deliver a rapidly changing payments landscape as increasing convergence, integration and e-commerce and mobile technology radically change the shape of the payments market place. Over the next five to seven years, retail and wholesale payments are expected to mature into highly automated and interactive eco-systems. Of particular importance, and a new opportunity for banks, will be the growth in the use of traditional electronic ACH payments in the retail sector. Electronic and the newly emerging alternative payments (e-AP)3 have an increasingly important role to play in enabling banks to displace cash and cheque transactions over the next decade as e-commerce grows and m payments accelerate rapidly.4 This new, wider vision also reflects a perception that convergence is taking place and that the differences between card and electronic payments (e-AP) will gradually decrease. The next decade is likely to see considerable investment and development to enable e-payments to be repositioned as universal payment instruments. However to meet the sophisticated needs of the retail sector e-AP will need gradual realignment to acquire the key acceptance, security5 and settlement attributes the banking community expects from modern payment methods at the POS, online and the mobile. Industry-wide collaboration will be needed to build a transformation road map to create a robust platform for the mass market uptake of these ‘next generation’ payment methods.

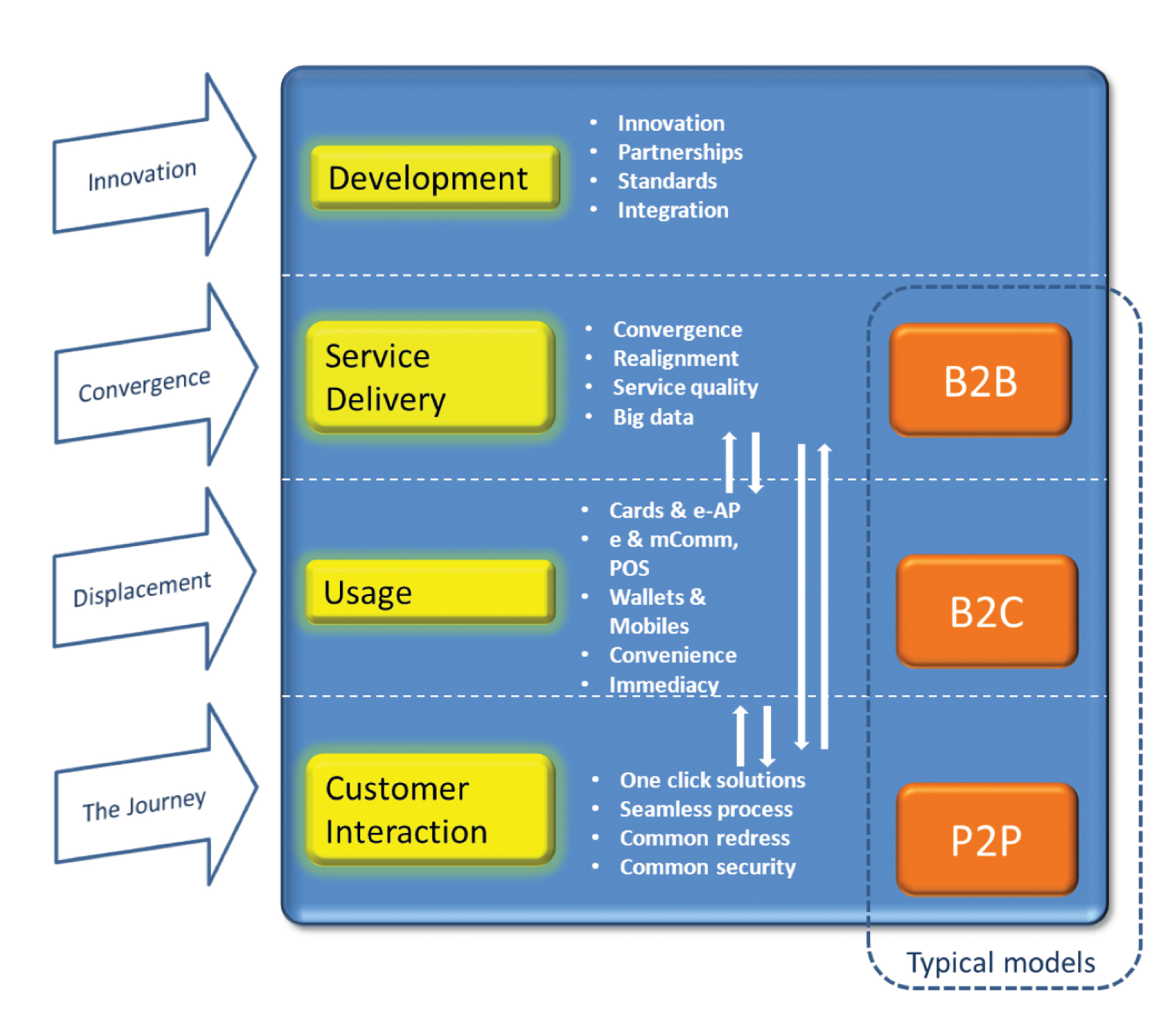

Click to enlarge

The key forces and factors influencing the development of payments eco-system today are illustrated in the diagram.

Individual and corporate personal computer and network processing capacity now delivered via smartphones and tablets will grow significantly in the future. Innovation and new developments plus partnerships, standards and integration will change the manner consumers, corporate and merchant customers behave, with most seeking seamless, one click solutions for all types of payment. Payments service delivery will increasingly converge and realign improving service and data while payments usage will be determined by convenience and immediacy. Interaction between banks and their customers will be defined by one click solutions, seamless processes and common redress and security.

Innovation and new developments will be the key drivers for change over the next five to seven years and the following assumptions have been factored into the new payments vision:

- That payments product and service proposition development will be customer journey driven and focus on interoperability and seamless provision.

- That payments innovation will continue to be driven by non-banks particularly in e- and m-commerce but that banks will partner with developers and use their innovative concepts and services to enhance traditional products and delivery.6

- That convergence in wholesale and retail payments will drive banks to migrate payments to in-house gateway based platforms reducing their reliance on P2P/bureau/third parties and enable banks to capture and secure corporate and merchant relationships.

- That as payment innovation expands banks will build flexible fast to market development delivery models for corporates and merchants many of whom will demand customised/ tailored solutions to meet their end customer’s requirements for integrated payments solutions.

Similarly the new payments vision has been built on the following payments service delivery assumptions:

- That the payments delivery landscape will evolve towards highly automated gateway platforms that will challenge the offerings of the traditional interbank ACH’s, processors and acquirers.

- That while many European banks will keep a focus on fee-based wholesale and retail businesses, some may not be able to keep up with innovation and change. The forward thinking will embrace the new technology, develop tailored solutions for vertical market sectors and use non-bank partners to help deliver the new and innovative payment solutions.

- That delivery of Big Data will be one of the keys to winning and successful corporate and merchant relationships with the use of powerful analytics engines and the delivery of data mining and visualisation services.

- That the end-to-end customer journey will be key to improving and retaining customer relations and will drive the quality of customer service.

- That back office processes will be extensively streamlined and automated to improve service support.

Key assumptions relating to the use of new payment methods are as follows.

- That Europe’s consumers will become more financially and technically sophisticated and will expect their buying experience to be characterized by an integrated customer journey enabling choice of selection, price comparisons and a seamless payment transaction (such as using an e-Wallet linked to a loyalty couponing programme).

- That the take-up of online and mobile payments will gather pace as more people become accustomed to personal banking via smartphone and tablet. Self-service channels will become highly developed with seamless interfaces into value added offers.

- That alternative payments will grow rapidly in e-commerce, mobile and at the POS and will gradually displace cash, cheques and other payment methods.

- That corporates will expect the same intuitive interface and simple functionality as retail customers to enable them to authorise payments, settle in real time and conduct trade finance transactions, including e-invoicing and will demand a fully consolidated view of their data and interactions at their bank(s).

- Key assumptions relating to banks, acquirers, consumers, corporates and merchants and their interaction with payments are as follows:

- That the proportion of transactions handled outside bank payments systems, while small in absolute terms, is expected to grow very rapidly7. Many forms of contactless and e- and m-payments will become mainstream, creating new use cases and threatening disintermediation of banks.

- That banks will extend their propositions and target to own the entire customer journey, not just part of the payments value chain. By this means banks may avoid their relegation to low value utility back office service and settlement providers.

That payment users will expect payments processing to be more responsive to their requirements and that end-users and corporate clients will leverage their market power with financial institutions and payment service providers to satisfy their payment needs.

For banks looking to sustain their payments business into the future, the first step towards a clear view of the emerging payments market is to understand the nature of the highly significant changes that are now underway. The underlying trend identified is that payment method and transaction convergence is gradually happening driven by customer demand for seamless one-click solutions. The focus of business propositions is shifting from product/silo orientation to client-orientation, where a common and high quality customer journey is an increasingly important component in the payments offer.

The ability of some banks to compete effectively against new entrants is currently undermined by a lack of appreciation of the outcomes of convergence and the needs of their customers and the highly disruptive impact of new payments concepts and services. Thus banks will need to speedily develop their payments strategy for the next decade if they are to avoid loss of payments market share to the growing numbers of non-bank players.

Bank customers require easy-to-use, bank-sponsored payments services that deliver a consistent experience, common redress and security. To achieve this, banks must gain a clear and holistic vision of the 2020 payments ecosystem and through a strategy of industry collaboration build robust platforms for the execution of the ‘next generation’ payments.

Footnotes

- World Payments Report 2013 by Cap Gemini/ RBS; WorldPay Insight Report on alternative payments; Mobile Money and the Battle for Consumer Engagement by Monitise.

- EBA commissioned PSE Consulting to conduct specific research in the areas of retail cash displacement and electronic and alternative payments.

- WorldPay Optimising your Alternative Payments – a Global Vision.

- The changing Face of Payments 2013 – Financial Services Club

- ECB Recommendations for the Security of Internet Payments 2012

- The Payments Innovation Jury Report 2013

- World Payments Report 2013