Securities Financing Transactions Regulation: danger signs

The aims of the Securities Financing Transactions Regulation (SFTR) may be laudable – but how much difference will some of the changes really make, other than create another operational burden? As Tracy Dilks, senior consultant, and Akber Datoo, founder and managing partner, D2 Legal Technology, suggest, the regulator might as well put a sign in the sea saying: “Danger – Water”.

Source: D2 Legal Technology

Shadow banking review

Concerns about the shadow banking market’s response to changing pressures, especially regarding the consequence of collateral reuse, have been growing. While the benefits of collateral reuse in improving liquidity and reducing funding costs are clear, the risks associated with increasingly complex collateral supply chains are a concern. The Financial Stability Board’s (FSB) recent recommendations are, in theory, designed to address the current lack of transparency regarding the extent to which financial instruments provided as collateral have been reused – and the associated risks. But will Article 15 SFTR really make any difference and help counterparties understand the risks better?

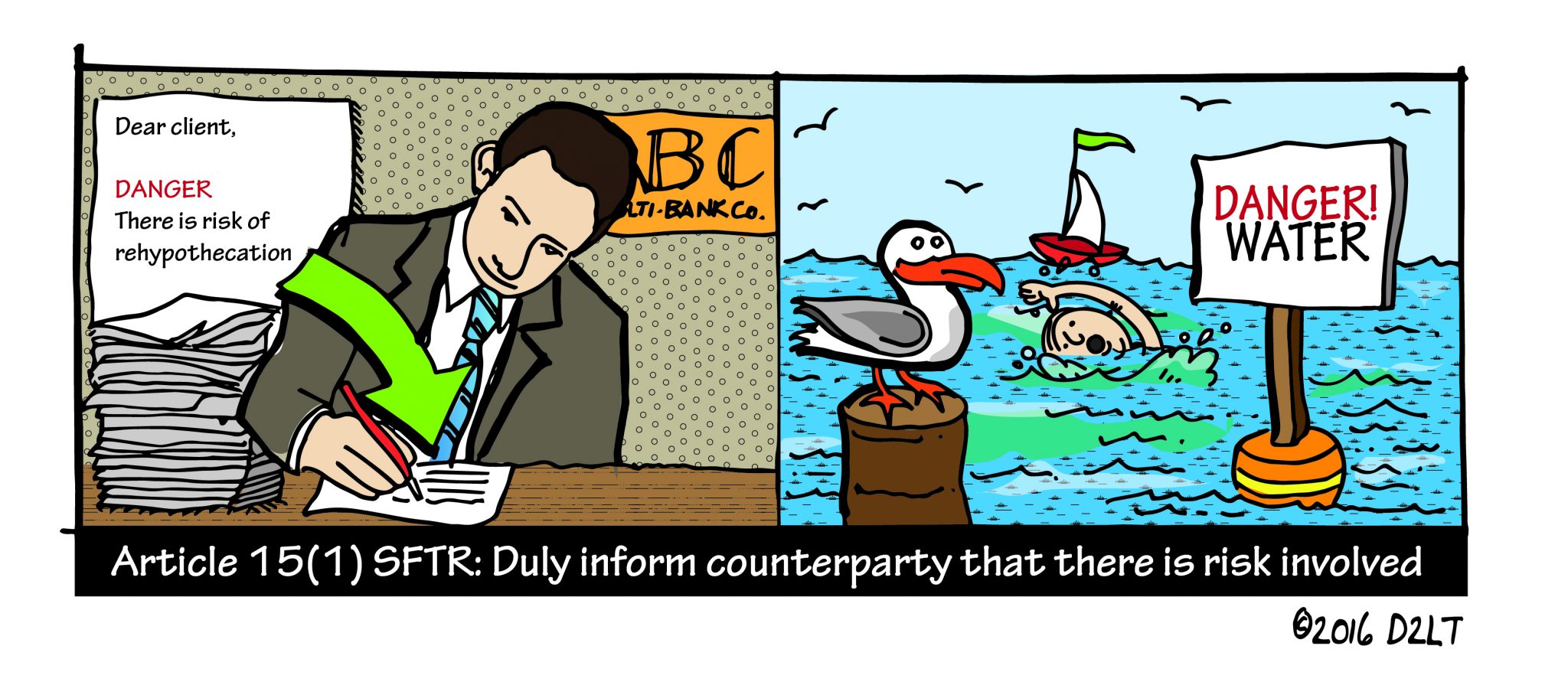

The regulation’s demand that all parties provide a notice stating that collateral transferred under certain securities financing transactions (SFTs) may be reused and the consequence of re-hypothecation sounds good in principle. But the reality is less compelling. The Article 15 SFTR Information Statement is merely a notice of collateral reuse risks and consequence. It cannot it be relied upon as legal, financial, tax, accounting or other advice nor is there an obligation for the recipient to formally acknowledge or accept the risks. So what additional value is it providing? It certainly does not deliver any specific warning or provide the supply chain with a better understanding of risk. In a sea of complex trades, Article 15 is no lifeguard – it is just another signpost stating that there may be some danger, somewhere, at some time. Not where; not when; and provides no help in identifying or mitigating that risk.

Laudable sentiment

In essence, the goal is to inform everyone in the complex supply chain. The wider SFTR requirements include new rules on reporting of securities financing transactions (SFTs) to trade repositories and demands disclosure by collective investment undertakings of their use of SFTs and total return swaps in their prospectuses and periodic reports. The SFTR also aims to implement FSB recommendations that financial intermediaries should provide clients with disclosure on the effects of re-hypothecation of client assets. The new EU rules will require all counterparties – not just financial intermediaries – to provide additional disclosures to the collateral provider if they receive financial instruments as collateral with a right of use or under title transfer arrangements.

Coming back to Article 15 however, the regulation simply requires the provision of a notice with standard wording to be applied in all situations. Documentation is not tailored to reflect the specific collateral reuse (in fact, the industry is busy debating the exact text to be churned out verbatim in each of these notices); and the sheer volume of notices going to every single party or counterparty (sell-side and buy-side) means that organisations are likely in practice to adopt a “receive and throw” mentality. When organisations are facing the issue of creating and/or receiving thousands of these notices – all with identical wording – the likelihood is that the good intention behind Article 15 SFTR (heightened awareness or refreshed awareness of rehypothecation) may be ignored.

Managing consent

The SFTR is clear that reuse of collateral must be undertaken in accordance with the terms specified in the collateral arrangements, i.e. that express consent must be given by the collateral provider to the collateral receiver to reuse the collateral. To satisfy this requirement the parties and counterparties need to track that the collateral arrangement’s provisions pertaining to consent of collateral transfer have not been amended to the contrary.

There are many complex provisions within the existing SFT agreements that could affect the right to re-use – for example, the rights to use that are contingent on a party maintaining certain credit ratings. As shown by a recent industry survey of financial institutions, more than 50% of market participants have no mechanism of tracking such terms, never mind ensuring that they abide by those terms upon a downgrade. Surely that is where the regulators need to focus, clamping down through fines and/or sanctions and ensure firms understand the seriousness and importance of tracking these conditions.

Conclusion

Once again, firms face another compliance burden – which will be significant – with no obvious upside. If the intention of SFTR is to change culture, build trust or mitigate risk, it is questionable that generating a standard notice to circulate amongst themselves will make any difference. Is it a notification or a warning, and if the former, to what end? Is this really the best, most appropriate way to share this information? Is it, more pertinently, going to have any impact on improving financial stability?

The existence of risk is not in question – the issue is whether Article 15 SFTR does any more than provide another red flag in a sea already full of flags. The recipients of the market, experienced players, are already swimming in the sea and warning them that there is water in the sea they swim in is simply helping no-one. The principles are noble but when there is so much regulatory change in the market, surely the goal should be to focus on activity that will have a tangible benefit, rather than adding operational complexity without any real upside?