Money market statistical reporting: challenges for 2016 and beyond

Nicos Kynicos, Senior Regulatory Reporting Specialist at Wolters Kluwer Financial Services

Money Market Statistical Reporting presents a fair number of challenges. And firms are pressed for time to prepare for these requirements, according to an overview prepared by Wolters Kluwer Financial Services. Where they may have adopted tactical solutions in the past to meet transaction level reporting obligations, now is a good opportunity to think more strategically about investing in the right platform and infrastructure. This is especially true given that daily reporting obligations will soon be extended in 2018 to include securities and financial transactions, writes Nicos Kynicos.

In 2014, the size of the Euro money market was estimated through the annual Money Market Survey (MMS) to be almost €80 trillion with 80% comprising of secured and unsecured lending, FX Swaps and Euro Overnight Index Swaps (OIS). In the UK, the Sterling Overnight Index Average (SONIA) is a critical benchmark referenced in £10 trillion OIS contracts and underpins the valuation of £35 trillion swap transactions. Given the importance that both these markets have within the European Union as well as the Global economy, policy makers are seeking to make changes to money market statistical reporting requirements that will enable them to have higher quality, granular and timely data on key Euro and UK Sterling money market segments so as to;

- provide relevant and timely data on the monetary policy transmission mechanism

- closely monitor monetary policy and financial developments

- inform market participants on market functioning to allow informed choice amongst reference rates

On 26th November 2014, the European Central Bank (ECB) adopted regulation (EU) No. 1333/2014 concerning statistics on the money markets (ECB/2014/48) and this was published in the official journal of the European Union on 16th December 2014. As a consequence in 2016, the European Union will see the introduction of two new major money market statistical reporting (MMSR) requirements. The first requirement relates to the Euro Money Markets and the second relates to the UK Sterling Money Markets.

Under these requirements reporting agents will be required to report daily transaction-by-transaction data with other monetary financial institutions (MFIs), other financial intermediaries (OFIs), insurance corporations, pension funds, central banks, the general government as well as transactions with non-financial corporations classified as ‘wholesale’ pursuant to the Basel III liquidity coverage ratio (LCR) framework directly to the European Central Bank (ECB) or National Central Bank (NCB) and the Bank of England (BoE) respectively.

The ECB will implement the daily reporting requirement in phases and has identified 53 significant entities to be included in phase 1 to start reporting in mid-2016 and phase 2 reporters to commence reporting a year later. The BoE has introduced two levels of reporting an annual report, which firms have just completed and a daily report. Based on the results of the annual survey, the BoE will define the daily reporting population such that the BoE capture data on 90% of the secured and unsecured sterling money market by way of total activity and total overnight activity. The BoE expects the daily reporting population to be in the region of 50 to 100 firms.

Broadly speaking the Euro and Sterling Money Market Statistical Reporting (MMSR) are very similar – the main differences being the currency and the fact that Euro MMSR also includes FX Swaps and Overnight Index Swaps. These additional instruments result in an additional 8 reportable fields in comparison to the Sterling MMSR, but this means there are 32 reportable fields which are the same. This is an important feature of both requirements, given that both the ECB and BoE have predetermined the reporting schemas that reporting agents will have to comply with will be aligned to ISO 20022 standards firms. As such firms should strive to create a single solution to both requirements in order to create efficiencies and cost savings.

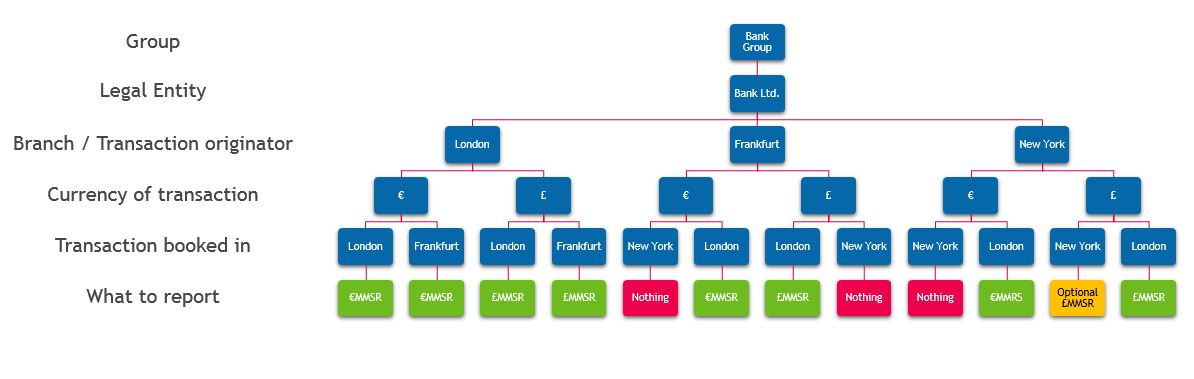

Operationally the impact of the requirements is broader than it may first appear – please see the diagram below. Firms need to understand how their global operations from a business and IT perspective are impacted by these requirements and define the optimal solution for them. Given the overlap between the reporting requirements firms should be thinking strategically – a single solution deployed centrally for both requirements. This approach may have higher upfront costs in terms of pooling data from different locations and systems, but it will deliver operational and financial benefits. In addition firms will need to have staff available to answer plausibility questions regarding the submission relating to day T from the relevant National Competent Authority (NCA) from 7am T+1 – this would be easier with a central deployment.

Daily MMSR presents significant challenges to institutions that will be part of the reporting population. Developing straight-through timely, high quality and accurate data submissions that will identify the appropriate reportable transactions will be critical. In addition many firms will find that they are in the reporting population for both of the daily MMSR reporting requirements discussed in this article – these separate requirements that have significant overlap, but also differences. Therefore selecting the right solution and partner that can implement quickly and will keep up to date with the reporting requirements as they change will be of paramount importance.