Core banking: true digital banking requires innovation on all layers

Peter-Jan Van de Venn, Five Degrees

By adopting a layered model that moves the focus from presentation to orchestration, banks can deliver an omni-access digital service that truly works for customers, says Peter-Jan Van de Venn, CCO of Dutch digital core banking platform provider Five Degrees.

Banks have undoubtedly grasped the importance of bringing digitisation to their customers. The extent to which banking has become consumer-centric and technology driven was one of the core topics discussed at last year’s British Bankers’ Association (now UK Finance) digital banking conference and the author of the Juniper Research report “Retail Banking: Digital Transformation & Disruptor Opportunities 2017-2021” refers to record levels of investment in banking technologies.

Many banks that have tried to digitise their services have started in the front layer with portals or apps. This approach may appear logical since this is the layer that the client sees, but all the other layers in the system have to be able to support it, which has huge cost implications.

In many cases, banks are running technology that is decades old. This not only prevents a good customer experience, but is also very costly to maintain. There is also a time to market issue in that banks have limited flexibility if they are relying on old systems to deliver new services.

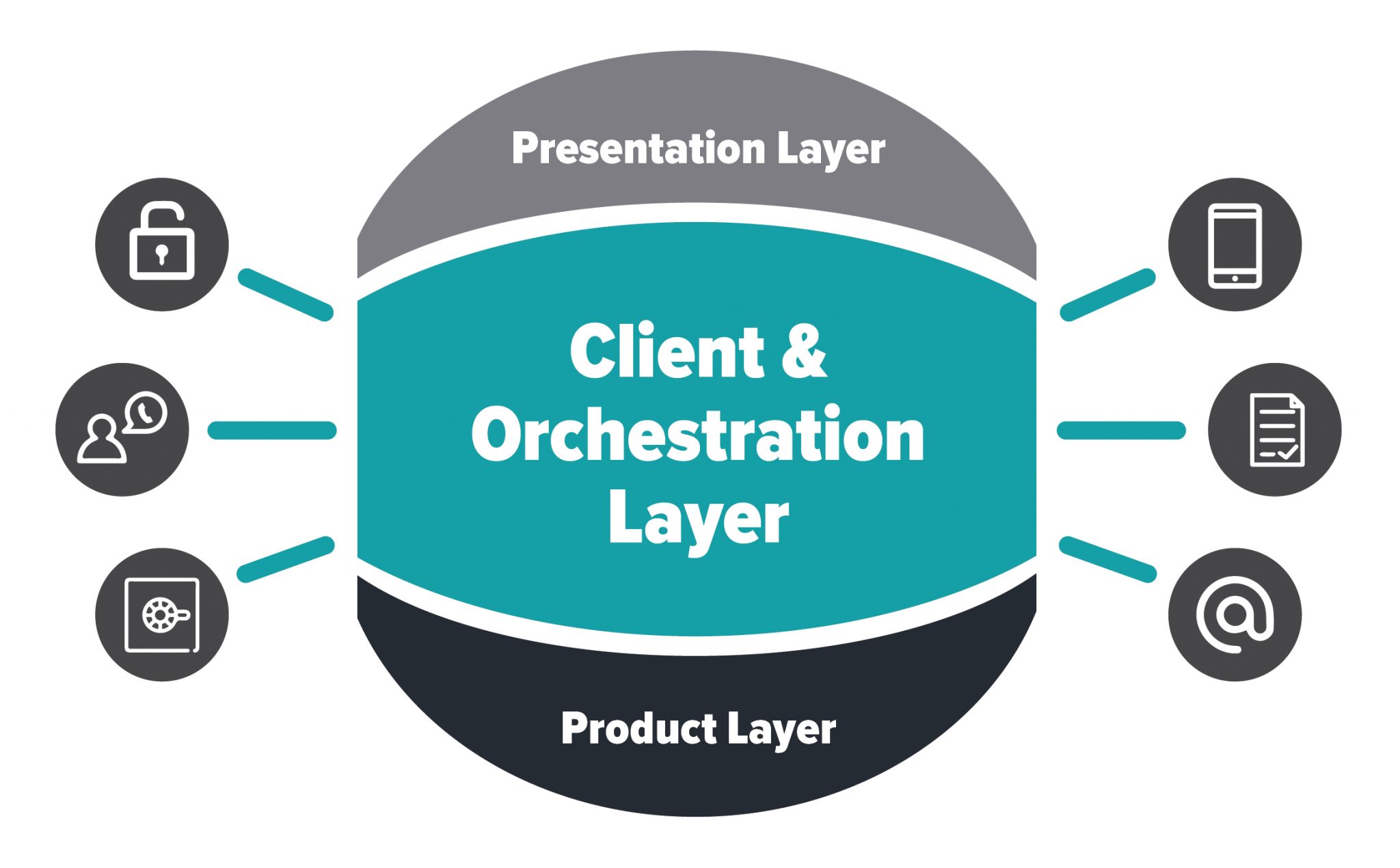

Our view is that it is more effective to focus on all three layers of the core banking platform – front, mid and back – or as we describe them the presentation layer, client and orchestration layer and product layer.

Customers increasingly expect a seamless customer experience from their bank. However, many banks have multiple back-ends for different types of product, which makes it difficult to achieve a single view of the customer for the bank and to provide the customer with a single view of all their accounts.

These multiple systems tend to mingle product and client information, which in our view needs to be separated into:

- A thin presentation layer of information for customers (and employees who also use the system).

- A client and orchestration layer focused on handling all client related processes and information – CRM, workflow management and communication – that orchestrates between the presentation layer, the back-end and the fintech ecosystem.

- A product layer focused on handling products, ideally containing no client information.

However, a true digital core banking system takes this process a stage further by using APIs rather than screens. Only APIs can provide the flexibility that is needed in the front or presentation layer. With services exposed to the “outside world” anybody can in principle access the services and (depending on their role) gain access to certain data and functionality. In this scenario the bank has moved beyond omnichannel to omni-access.

At the client and orchestration layer, APIs unlock the potential of the fintech world, enabling customers to make use of providers developing niche services for know your customer (KYC) or data analytics, for example. With this system there is no need for repeated onboarding of the same customer, which also improves the customer experience.

It is tempting for banks to wonder how they can ever update their spaghetti of legacy systems and to be concerned that by the time they have updated their systems, the technology will already be obsolete.

This is where non-coded configuration comes in. Processes are adjustable in the client and orchestration layer and products are configurable in the back layer, meaning banks can make changes and introduce new products and services in a matter of weeks rather than months.

We have outlined above some of the reasons why digital transformation on legacy systems is a flawed strategy for large banks. The answer lies in the greenfield approach that a number of large banks have adopted, setting up new operations alongside their existing businesses.

These new entities are often managed by young, talented people with a mandate to deploy new technology. In many cases they operate out of different buildings and have direct reporting lines to the executive board in order to not be influenced by any organisational legacy, which can be even more limiting than IT legacy. The objective is that new customers will even onboard themselves from the old to the new bank.

Having a great website or app does not make you a digital bank. It also requires the implementation of next generation software in the mid and back layer to provide the customer experience that customers already expect – and receive – from other service providers.

This article is also featured in the November 2017 issue of the Banking Technology magazine.

Click here to read the digital edition – it is free!